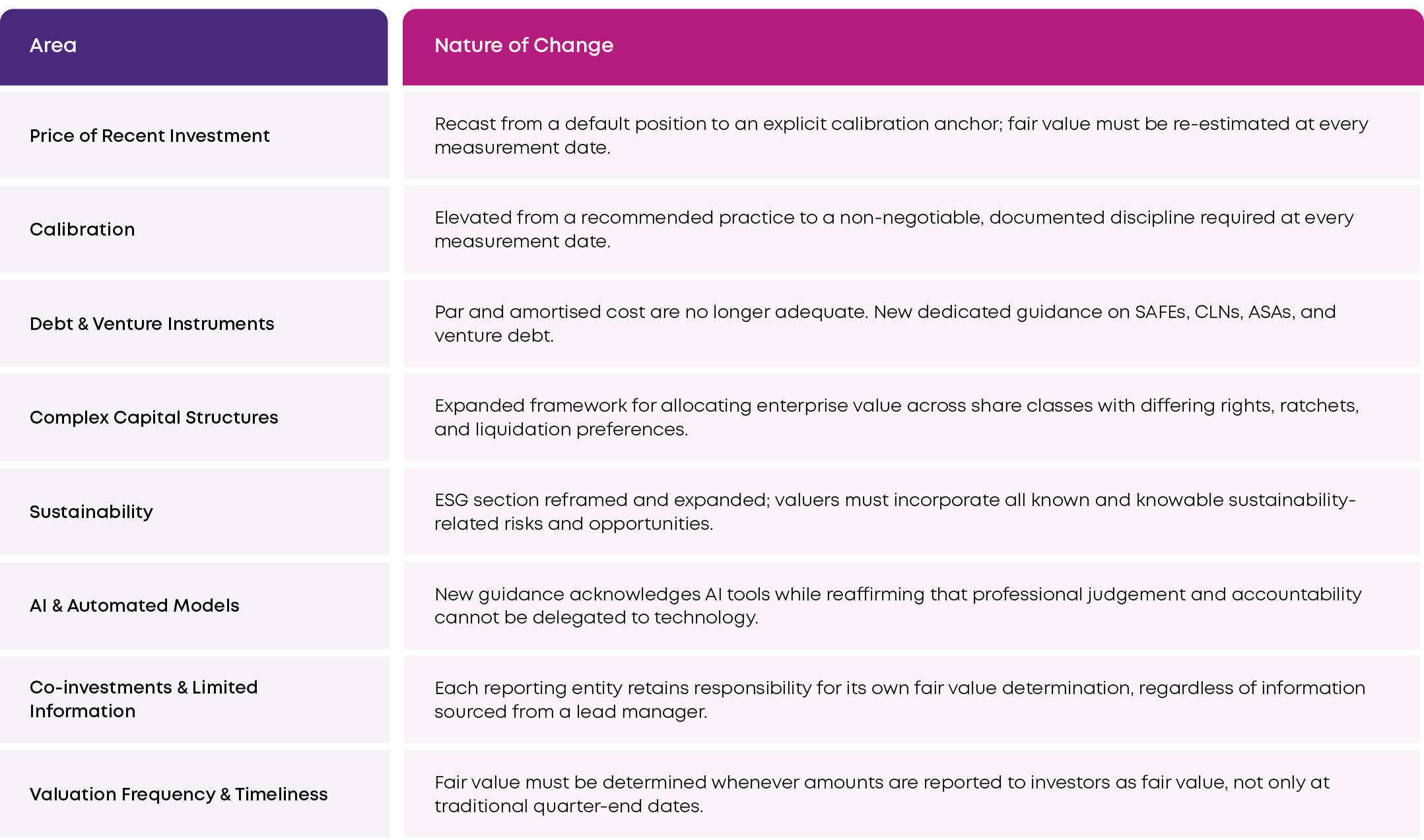

Key Changes in the 2025 Guidelines

The 2025 Guidelines address eight substantive areas. Some represent clarification of existing principles; others introduce new or expanded guidance that will require firms to revisit their current approach.

Price of Recent Investment

In earlier editions of the Guidelines, the price of a recent investment (PoRI) was widely understood — if not always explicitly endorsed — as a reasonable proxy for fair value in the period immediately following a transaction. The 2025 Guidelines clearly recast this position.

PoRI, when deemed to represent fair value, is now positioned as a calibration anchor rather than a valuation technique in its own right. More significantly, the 2025 edition states explicitly that fair value must be re-estimated at each measurement date, even when a recent transaction exists. Prior prices cannot be carried forward unless they remain consistent with current market participant views at the reporting date. For many firms, this will require a more deliberate analytical step, where previously a price might simply have been held.

Calibration

The concept of calibration is not new to the IPEV Guidelines, but its treatment in the 2025 edition elevates it from a recommended analytical discipline to an explicit requirement. Calibration — the process of ensuring that a valuation technique and its inputs are consistent with observable market data, most notably an observed transaction price — must now be applied and evidenced at every measurement date.

In practice, this means maintaining a clear analytical bridge from an observed transaction price (whether at entry or from a more recent orderly transaction) to the fair value conclusion at the current date. The 2025 Guidelines provide more structured guidance on the elements of a well-executed calibration:

- The entry transaction price is used to back-solve the inputs — such as EBITDA multiples, discount rates, or revenue growth assumptions — implied by the original transaction. This establishes the anchor.

- At each subsequent measurement date, the valuer documents how and why those inputs have evolved, using a coherent framework that tracks both company-specific developments and movements in comparable market benchmarks.

- Methodology should be consistent from one reporting date to the next. Where the approach changes, that change must itself be explained and documented.

- Where more recent orderly transactions exist — whether in the portfolio company itself or in comparable businesses — calibration should anchor to those rather than to an earlier transaction.

- Mechanical roll-forwards and formula-driven updates are explicitly cautioned against. Calibration is structured professional judgement, not a process that can be reduced to a formula.

The Guidelines note that calibration is most directly relevant when the measurement date is close to the transaction date. Still, they also affirm its value — as a consistency check on the evolution of unobservable inputs — even when substantial time has passed since the original transaction.

ON CALIBRATION AND FREQUENCY

One practical consequence of the calibration framework is that it provides a structured basis for interim valuations without requiring a full re-assessment at each reporting date. A well-documented calibration at the annual or semi-annual date establishes an analytical reference point from which subsequent interim updates can be conducted as structured, evidence-based adjustments. This does not reduce the substantive requirement at interim dates — fair value must still reflect a genuine assessment — but it provides a methodology that scales across reporting frequencies without a proportionate increase in workload.

Debt, Venture Debt, and Convertible Instruments

The 2025 Guidelines reorganise and expand the guidance on debt to make explicit what was previously implicit: par, face value, and amortised cost are not adequate proxies for fair value, and credit instruments should be valued using market-based yields, spreads, and expected cash flows wherever possible.

A new dedicated section addresses venture debt and convertible instruments — including SAFEs, convertible loan notes (CLNs), and advance subscription agreements (ASAs). These instruments are increasingly prevalent in venture and growth equity portfolios, yet have not previously received detailed treatment in the Guidelines. The 2025 edition provides direction on calibrating initial fair value to transaction terms, separating debt and equity components where relevant, and updating valuations as credit quality, optionality, and market benchmarks evolve. For many valuation teams, this will represent a material change in the depth of analysis applied to instruments that have historically been carried at cost or face value.

Complex Capital Structures and Liquidation Preferences

Expanded guidance on complex capital structures introduces a more structured framework for two related challenges: determining whether a transaction price represents fair value across all share classes, and allocating enterprise value among classes with differing rights, preferences, and economic exposures.

The 2025 Guidelines pay particular attention to liquidation preferences, ratchets, and similar structural features that are common in venture and growth equity rounds. These features can create significant divergence between the economic position of different shareholders at a given enterprise value — a divergence that valuation techniques must reflect if they are to represent fair value from a market participant’s perspective. The updated guidance seeks to align valuation practice more closely with the analytical framework that sophisticated investors use to evaluate pay-off profiles across a capital structure.

Sustainability

The former ESG section has been reframed as ‘Sustainability’ and expanded materially. The 2025 Guidelines move beyond a general acknowledgement that ESG factors may be relevant to a more specific expectation: valuers must incorporate all known and knowable sustainability-related risks and opportunities, ensuring that fair value reflects both downside exposures and value-creation initiatives with measurable impacts.

The practical implication is that sustainability is no longer a box to be acknowledged and set aside. Where environmental, social, or governance-related factors have a plausible and quantifiable effect on projected cash flows or discount rates — even if they are not separately labelled as such in management forecasts — they should be reflected in the valuation. Valuers may increasingly be expected to demonstrate, in their documentation, that sustainability factors have been considered and either incorporated or consciously excluded with explanation.

Artificial Intelligence and Automated Valuation Models

For the first time, the IPEV Guidelines explicitly address the use of AI tools and automated valuation models in the valuation process. The treatment is measured: the 2025 edition acknowledges that such tools are increasingly used to source data, analyse comparable transactions, and perform calculations — and does not discourage their use.

The Guidelines are unambiguous; however, AI tools cannot replace professional judgement and scepticism. Valuers remain fully accountable for the inputs they select, the processes they apply, and the conclusions they reach — including when AI has assisted in generating data or performing analysis. This accountability cannot be delegated to a model or a platform.

For valuation teams that have begun to incorporate AI tools into their workflows — or are considering doing so — this guidance provides a useful framework: use technology to augment and accelerate, but ensure that the professional responsible for the valuation has genuinely engaged with and can defend every material judgement embedded in the conclusion.

Co-investments and Limited Information Preferences

Section II 5.18 of the 2025 Guidelines addresses a situation that has become increasingly common: investors with limited information rights, or those holding co-investments alongside a lead manager. The guidance is clear that the responsibility for determining fair value rests with each reporting entity, regardless of the information-sharing arrangements in place.

Co-investors may use information provided by the lead investor as input to their own valuation process. Still, they may not treat it as a substitute for independent valuation judgment. The Guidelines also note that where information risk is elevated — due to restricted access to portfolio company data — this may itself be a factor that justifies higher required returns and, consequently, lower fair values. For co-investment vehicles, these points have direct implications for how valuation processes are designed and documented.

Valuation Frequency and Timeliness

The most direct signal in the 2025 Guidelines of where market expectations are moving is the updated treatment of valuation frequency. The Guidelines now explicitly state that fair value must be determined whenever amounts are reported to investors as fair value. This formulation is intentionally broader than the traditional quarterly cycle.

This change acknowledges a reality that many managers are already navigating LPs, fund administrators, secondary buyers, and regulators are increasingly requesting valuations — or at least valuation-grounded portfolio data — at intervals that do not align neatly with quarter-end reporting cycles. By framing frequency as a function of when fair value is reported rather than when a standard reporting period ends, the 2025 Guidelines place the responsibility on managers to ensure their valuation processes can respond to those demands.

Implications for Valuation Practice

The changes described above have implications across three dimensions: the technical conduct of valuations, the processes and governance that surround them, and the expectations of the various stakeholders who rely on the outputs.

Technical Implications

For valuation specialists, the 2025 Guidelines require a more disciplined approach to evidence and documentation at the individual investment level. Deal-level files will need to demonstrate a coherent analytical bridge from entry pricing — or from the most recent comparable transaction — to the current fair value conclusion, with explicit explanation of how market inputs and company-specific factors have evolved.

The expanded treatment of debt instruments, convertible securities, and complex capital structures will require more sophisticated models for instruments that have historically received lighter analytical attention. Valuers working across venture and growth equity portfolios in particular will need to ensure they have both the technical tools and the sector knowledge to apply the updated guidance on venture debt, SAFEs, and pay-off analysis across complex share class structures.

Sustainability integration will require valuation teams to develop a more systematic approach to identifying and quantifying environmental, social, and governance factors—not as a separate exercise but as a component of the core valuation analysis.

Process and Governance Implications

From a process perspective, firms should expect to revisit their valuation policies to reflect the 2025 Guidelines’ updated expectations. Topics requiring policy-level attention include: the treatment of ‘known and knowable’ information and the point at which it must be incorporated; the documentation requirements for calibration at each measurement date; the standards applied to sustainability factors; the governance framework for AI tool usage; and the approach to co-investment situations.

Governance, more broadly, will need to reflect the higher evidentiary bar set by the 2025 Guidelines. Independent review, structured documentation, and systematic back testing of valuation assumptions are not new concepts — but the 2025 edition makes clearer that these are expected elements of a credible valuation process, not optional enhancements. The ability to demonstrate that valuations are subject to genuine challenge and continuous improvement, rather than mechanical repetition, will become increasingly important in discussions with auditors, regulators, and LPs.

Stakeholder Implications

For managers, boards, and CFOs, the practical effect of the 2025 Guidelines is a higher bar for evidencing the transparency, consistency, and defensibility of fair value estimates — both at the individual investment level and across the portfolio as a whole. The more structured treatment of calibration, frequency, and documentation provides a clearer benchmark against which auditors and regulators can assess whether valuation practice meets recognised standards.

For LPs and their advisers, the changes offer greater assurance of consistency and comparability across managers and reporting periods. The explicit treatment of valuation frequency and the calibration framework together point toward a world in which LP reporting is grounded in more current, more auditable data — even if the destination remains farther away than the guidelines alone can take us.

Two topics will feature with greater regularity in conversations between valuers, managers, and their stakeholders going forward:

- Sustainability: Valuers will be expected to demonstrate that they have genuinely considered sustainability impacts where relevant — and to explain how those considerations, as applicable, are or are not reflected in their assumptions.

- AI and technology: As AI tools become more prevalent, the question of how they are used, what oversight is applied, and where accountability for the conclusion rests will become a standard element of valuation governance discussions.

Looking Ahead: Towards Continuous Portfolio Monitoring

The 2025 IPEV Guidelines do not describe a future state for private markets valuation — they refine the standards applicable to the present. But read carefully, and in the context of the direction LP and regulatory expectations are taking, several of the changes point toward a practice that looks meaningfully different from the quarterly, largely backward-looking cycle that has characterised the profession.

The elevation of calibration to a non-negotiable discipline at every measurement date, combined with the explicit linkage of valuation frequency to LP reporting rather than fixed calendar intervals, creates a methodological and regulatory foundation for more continuous engagement with portfolio fair value. The calibration framework — with its emphasis on a documented anchor point and a structured process for updating that anchor as market and company conditions evolve — is well suited to a world in which interim valuations are expected to be substantive rather than perfunctory.

The acknowledgement of AI tools, while carefully bounded by an unambiguous restatement of professional accountability, implicitly recognises that the data-intensive aspects of valuation — tracking comparable market multiples, monitoring portfolio company KPIs, identifying relevant transactions — are increasingly amenable to technological support. The Guidelines do not prescribe how that support should be organised. Still, by affirming that it can legitimately be used, they open the door to valuation processes that are more responsive to market developments than a quarterly cycle permits.

The direction of travel, taken as a whole, points toward a valuation practice characterised by greater frequency, greater consistency, and greater transparency — one in which portfolio fair values are maintained on a more continuous basis and in which LPs have access to more current and more auditable information than periodic reports have historically provided. The technology to support such a model is increasingly available; the methodological framework is taking shape; what the profession now needs to build is the governance architecture that connects the two.

For valuation professionals, this represents an evolution in role as much as in method. As the more mechanical aspects of the valuation process are progressively supported by technology, the premium on skilled professional judgement — on interpreting complex situations, setting and maintaining analytical frameworks, and providing the independent sign-off that gives a fair value conclusion its credibility — rises rather than falls. The 2025 Guidelines, with their insistence on documented judgment and calibration discipline, are already pointing the profession toward that higher-value function.

“The firms best positioned for this future are those that treat the discipline the guidelines require — rigorous calibration, documented judgement, consistent methodology — not as a compliance burden, but as the foundation of a genuinely robust valuation practice.”