The Data Center Boom: Scale, Scope, and Strategic Context

The Investment Landscape

The numbers are staggering. S&P Global research indicates that data center and AI-related investments accounted for approximately 80% of U.S. private domestic demand growth in the first half of 2025 . Data center construction spending in the U.S. has grown at a CAGR of approximately 98% since 2021 —effectively doubling every year. The average cost per data center facility now approaches $600 million, with per-square-foot costs nearing $1,0006.

This investment wave extends far beyond the United States. Europe, while trailing the U.S. in current spending, is scaling rapidly with a $500+ billion pipeline, led by key hubs such as Frankfurt, London, Paris, and Amsterdam under increasingly stringent energy regulations.

Asia-Pacific is set to nearly double capacity by 2030, driven by investments in Japan, Southeast Asia, and India—with government initiatives accelerating growth across Mumbai, Chennai, and Hyderabad. Meanwhile, the Middle East—particularly the Gulf States—is emerging as a strategic AI hub, backed by sovereign capital and strong colocation investment momentum.

Capital Allocation Breakdown for Data Center Investments

The Chip Revolution Fueling the Boom

NVIDIA’s GPU evolution illustrates the pace of change: the Ampere architecture (A100, 2020) delivered the first generation of purpose-built AI training GPUs. The Hopper architecture (H100/H200, 2022–2023) introduced the Transformer Engine. The Blackwell architecture (B200/B300, 2024–2025) represents a generational leap with 208 billion transistors and up to 15x the inference performance of the H100. NVIDIA’s roadmap extends to the Rubin architecture (2026+).

NVIDIA GPU Architecture Evolution: Accounting Implications

This relentless cadence of innovation—roughly 18 to 24 months between generations—has profound implications for useful life assessments and impairment analysis, as summarized below:

- Companies evaluating AI infrastructure investments, the technology lifecycle is not just an engineering consideration—it is the single most consequential input into depreciation policy, impairment testing, and useful life governance.

- Uniqus support clients in building technology-aware accounting frameworks that translate chip roadmaps into defensible financial reporting judgments.

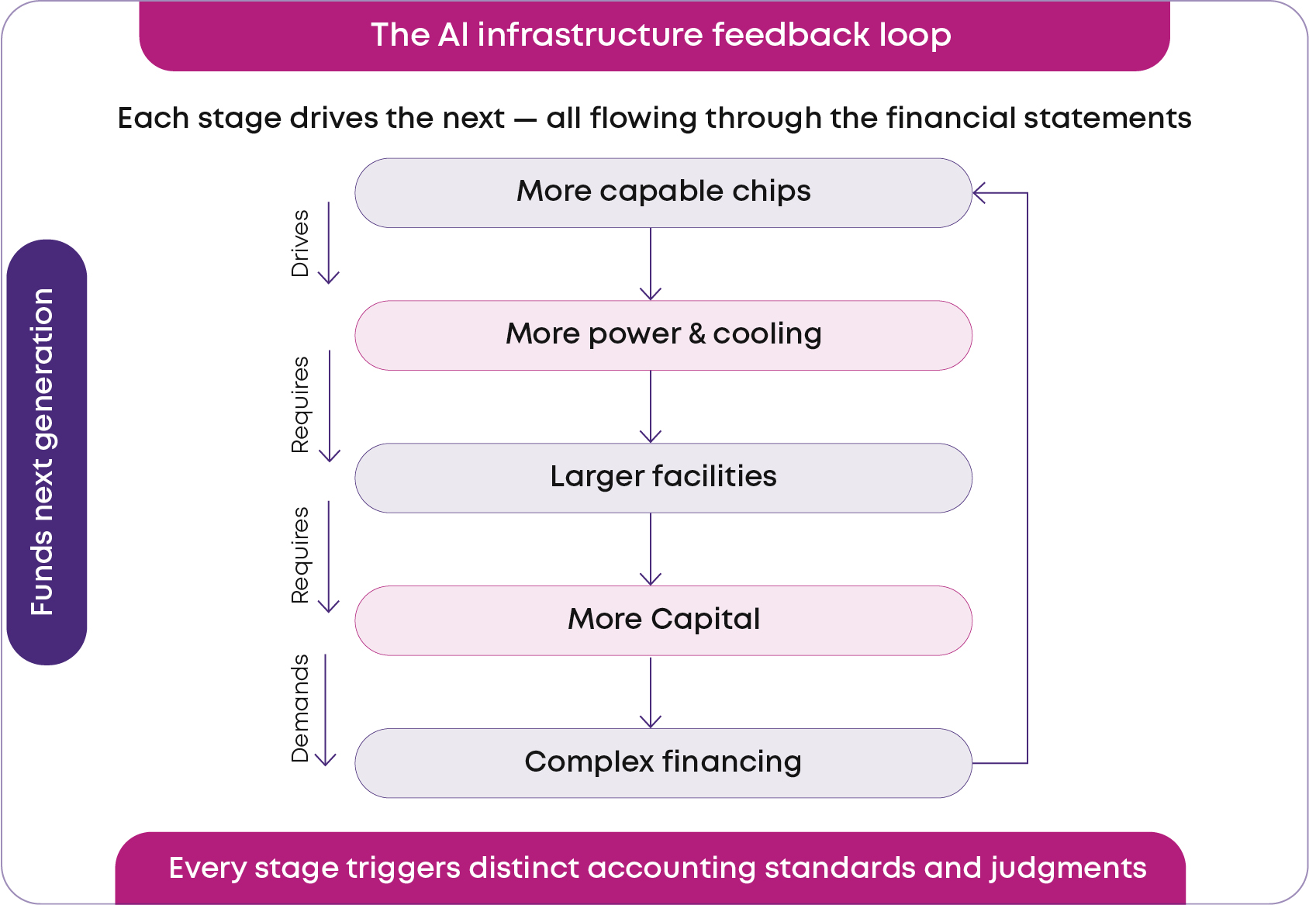

How Data Centers Power AI and Machine Learning

Modern AI workloads—training large language models (LLMs), running real-time inference, processing multimodal data—require fundamentally different infrastructure than traditional enterprise computing. Training a single frontier AI model now requires thousands of GPUs operating concurrently, consuming 25+ megawatts of power over weeks or months. The shift from inference-light to inference-heavy workloads (driven by AI reasoning models and agentic AI) is further amplifying demand for specialized, high-density computing environments.

This creates a feedback loop

Finance leaders must understand this feedback loop because every stage of it triggers distinct accounting questions—from capitalization and depreciation, lease classification, complex financing and environmental obligations.

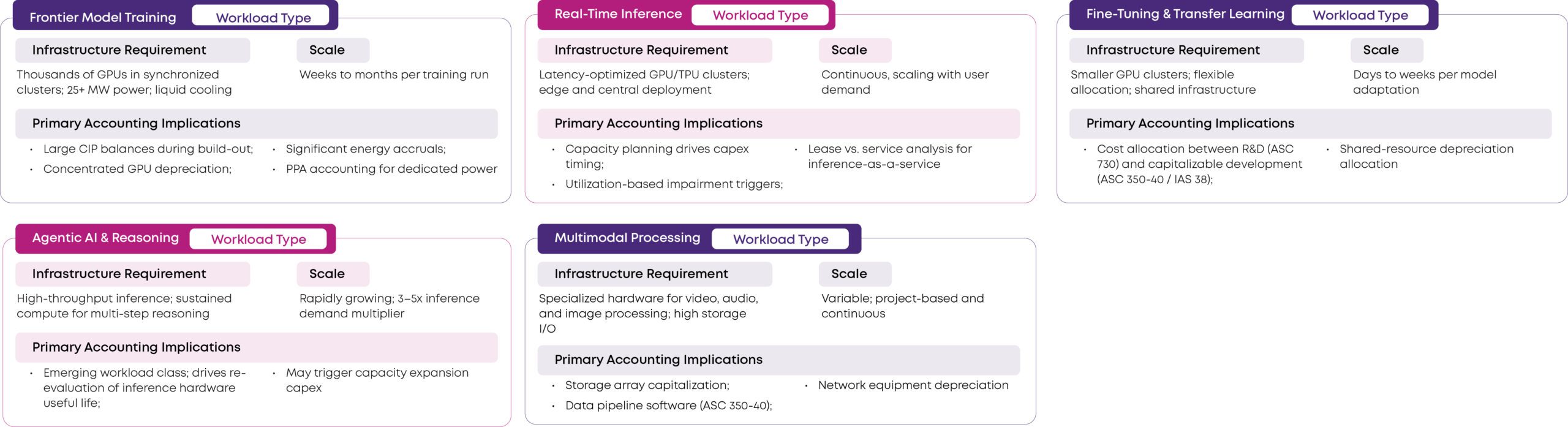

AI Workload Types and Their Infrastructure Accounting Implications

Specific Accounting Considerations

1. Capital Expenditure: Accounting for the Build Context

1.1 Capitalization Framework Under US GAAP

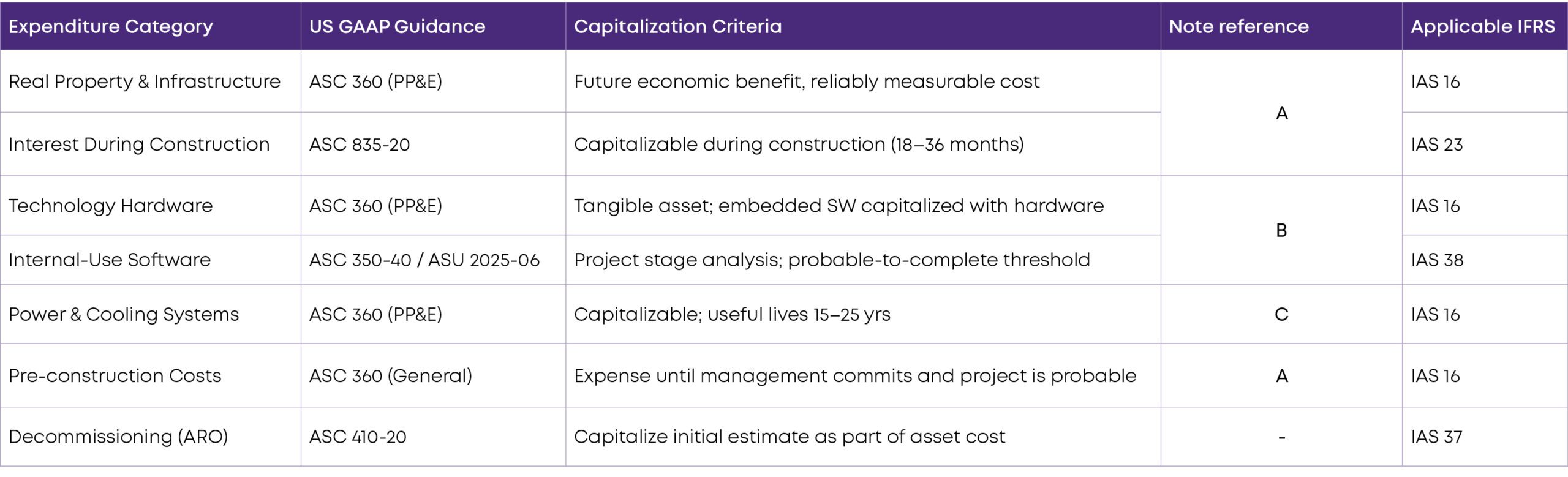

Data center construction involves multiple categories of expenditure, each governed by different capitalization guidance under US GAAP. Understanding these distinct frameworks is critical for accurate financial reporting.

Capitalization Framework: Multi-Standard Mapping

To know more about the notes, download PDF.

1.2 Costs Frequently Overlooked or Misjudged

Following are some of the key considerations where capitalization judgments are commonly challenged:

Recommended Actions

- Update capitalization policy to specifically address data center asset categories, thresholds, and cost allocation methods. Include specific guidance for pre-construction costs, redundancy systems, and commissioning.

- Perform a formal component identification and grouping exercise for all existing and planned data center assets. Document significant components with distinct useful lives.

- Design process for tracking qualifying construction projects, weighted-average accumulated expenditures, and capitalizable borrowing costs under ASC 835-20 / IAS 23.

- Evaluate impact of ASU 2025-06 (probable-to-complete threshold) on internal-use software capitalization for proprietary AI orchestration and workload management platforms.

2. Depreciation and Useful Life: The Hardest Judgment Call

Even when capitalization is appropriate, determining useful life is fraught with judgment.

AI technologies face:

Determining useful life becomes judgment intensive. Amortization periods that are too long may overstate earnings. Periods that are too short may introduce unnecessary volatility.

Organizations must consider:

Periodic reassessment is not optional — it is expected.

Key considerations

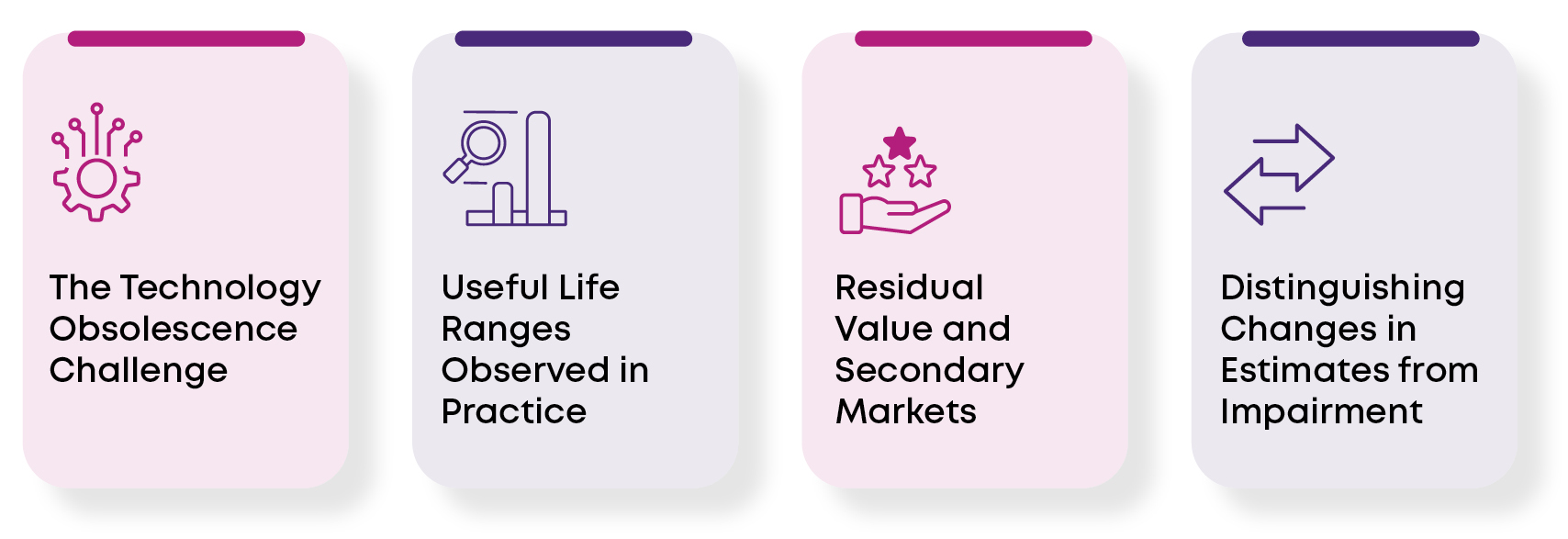

2.1 The Technology Obsolescence Challenge

- One of the most significant accounting judgments in data center reporting is determining the appropriate useful life of technology assets.

- The rapid pace of innovation—particularly with GPU generations evolving on approximately 18–24 month cycles—intensifies this assessment. For example, an H100 GPU acquired in early 2023 may remain fully functional in 2025, yet deliver lower performance-per-watt compared to newer alternatives such as the B200, making it less economically efficient for advanced workloads.

- This dynamic creates a clear distinction between:

- Physical useful life – the period over which the asset remains operational; and

- Economic useful life – the period over which the asset generates acceptable returns relative to newer technologies.

- Under ASC 360-10-35, useful life is an entity-specific judgment — based on how the reporting entity intends to use the asset, not solely its physical durability or its economic life from a market-participant perspective. For GPU and AI accelerator hardware, where technology refresh cycles are significantly shorter than physical life, the entity’s planned replacement strategy and workload requirements are the primary determinants.

- In determining economic useful life, entities should consider key factors such as physical wear and tear, technological obsolescence, and any legal or contractual constraints.

2.2 Useful Life Ranges Observed in Practice

Useful life assumptions for data center assets can vary significantly across categories, reflecting differences in technology cycles and operational use:

The table represents a synthesis of hyperscaler 10-K disclosures, industry lifecycle data, and practitioner experience. It is not drawn from a single source but rather reflects the observable range across the industry

These ranges are not merely theoretical—they reflect real differences in business models, usage patterns, and technology strategies across industry participants:

– For instance, a hyperscaler focused on frontier AI training workloads may adopt a shorter depreciation horizon (e.g., ~3 years for GPUs) due to rapid obsolescence, whereas a colocation provider serving enterprise workloads may reasonably apply longer useful lives (e.g., 5–6 years) for similar hardware.

- The variation in useful life assumptions has important accounting implications, particularly for depreciation patterns, earnings profiles, and comparability across entities-

- Shorter useful lives (e.g., for hyperscalers) accelerate depreciation, increasing near-term expenses and better reflecting rapid technological obsolescence

- Longer useful lives (e.g., for colocation providers) defer expense recognition and smooth earnings but may increase the risk of future impairments if assets become obsolete sooner than expected.

- In our view determining useful life under ASC 360 is a critical judgment that should align with an entity’s business model, asset utilization, and exposure to technology cycles, with clear disclosures to support comparability.

- Uniqus supports clients in establishing robust and consistent useful life frameworks for data center assets, aligned with technology cycles, business models, and accounting requirements.

2.3 Residual Value and Secondary Markets

- Emerging secondary markets: A growing resale ecosystem for used data center equipment (including servers and GPUs) is developing, with participation from operators and broker-dealers.

- Impact on depreciation: The existence of active secondary markets may support the assignment of residual values, thereby reducing annual depreciation expense.

- Need for reassessment: Given the high volatility in residual values driven by rapid technology cycles, entities should reassess these estimates periodically in accordance with ASC 360.

Distinguishing Changes in Estimates from Impairment

- Technology-driven obsolescence: The introduction of a new GPU generation may render existing hardware economically suboptimal, requiring management to reassess its accounting treatment.

- Distinguishing accounting outcomes: Management must evaluate whether the change reflects a revision in useful life (accounted for prospectively under ASC 250) or indicates a potential impairment trigger under ASC 360-10-35.

- Recoverability assessment: The critical consideration is whether the carrying amount of the asset group exceeds its undiscounted future cash flows.

- Outcome-based treatment: If the asset continues to generate reasonable—albeit reduced—returns, a revision to useful life may be appropriate. However, if the underlying economics have significantly deteriorated, an impairment test is required.

- Prospective estimate revision: Changes in useful life are treated as changes in accounting estimates and applied prospectively, impacting future depreciation expense without restating prior periods.

- Impairment trigger evaluation: Indicators such as technological obsolescence or reduced economic viability may trigger a recoverability test under ASC 360.

- Two-step impairment approach: If undiscounted cash flows are insufficient to recover the carrying amount, the asset group is written down to its fair value, with the loss recognized in earnings.

- In our view entities should establish processes to continuously monitor technological shifts and market conditions to ensure timely identification of estimate changes versus impairment triggers.

- Uniqus supports clients in identifying changes in accounting estimates and impairment triggers for data center assets by implementing robust assessment frameworks aligned with evolving technology cycles, asset utilization patterns, and applicable accounting standards.

IFRS Perspective:

Under IFRS, the accounting for depreciation and useful life is governed primarily by IAS 16 and IAS 36, with a strong emphasis on principles-based judgment and continuous reassessment.

- Useful life determination: Similar to U.S. GAAP, assets are depreciated over their economic useful lives, considering factors such as expected usage, technological obsolescence, physical wear and tear, and legal or contractual limits.

- Mandatory periodic reassessment: IFRS explicitly requires entities to review useful lives, residual values, and depreciation methods at least annually, with any changes treated as changes in accounting estimates and applied prospectively. This creates a higher expectation of ongoing reassessment compared to practice in some U.S. GAAP environments.

- Impairment framework: Under IAS 36, impairment testing is based on a single-step recoverable amount approach, defined as the higher of value in use (discounted cash flows) and fair value less costs of disposal. This differs from the U.S. GAAP undiscounted cash flow recoverability test and may result in earlier identification of impairment indicators in rapidly evolving technology environments.

Overall, while the core principles are broadly aligned with U.S. GAAP, IFRS frameworks tend to be more dynamic and judgment-driven, with greater emphasis on periodic reassessment, residual value estimation, and earlier impairment recognition—all of which are highly relevant in the context of AI-driven data center investments.

Recommended Actions

- Annual full review of useful lives + quarterly trigger monitoring.

- Build depreciation sensitivity models for each asset cohort (±1-year useful life change). Present to Audit Committee quarterly. Quantify EBIT and margin impacts.

- Establish relationships with equipment resellers (e.g., Iron Mountain, broker-dealers) to obtain secondary market pricing data. Integrate into residual value assessments.

- Design quarterly trigger assessment incorporating: GPU roadmap updates, utilization rates, secondary market prices, peer disclosures, and customer demand signals.

- Compile and maintain database of hyperscaler and DC operator useful life disclosures. Update with each 10-K filing cycle. Use for audit defense and policy calibration.

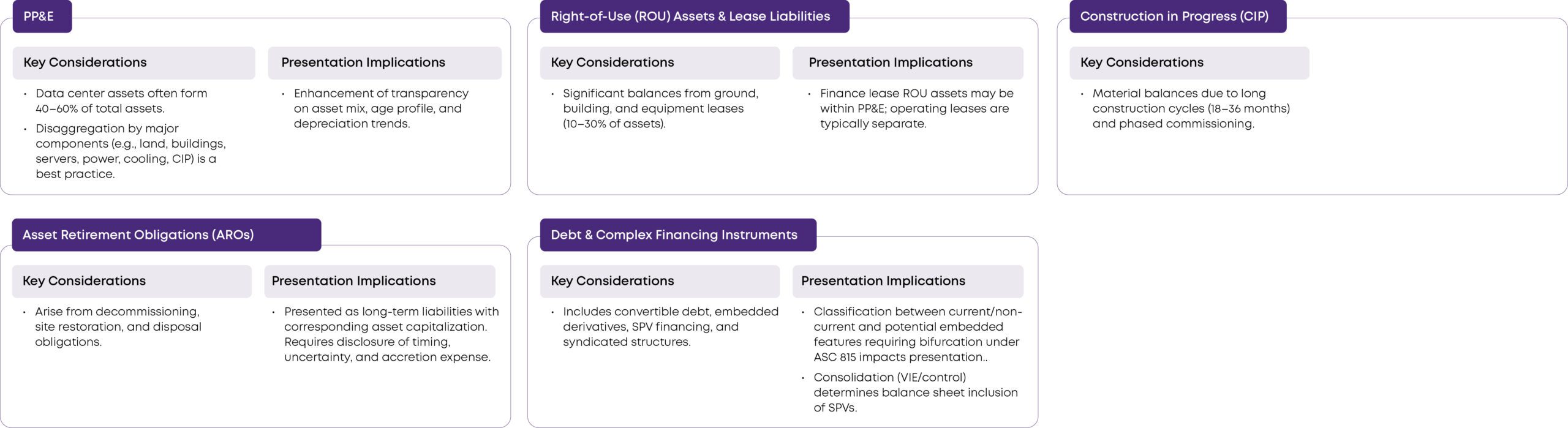

3. Financing the Data Center Boom: Complex Instruments and Their Accounting

The sheer scale of data center investment has driven innovation in financing structures. S&P Global reports that debt issuance for data center purposes nearly doubled to $182 billion in 2025, while lenders committed $121 billion in credit for U.S. data center properties alone. Understanding these structures and their accounting implications is critical for accurate financial reporting

3.1 Financing Structures: Accounting Treatment Matrix

To know more, download PDF.

- Increasing complexity in financing structures: The financing ecosystem surrounding data centres have evolved significantly, often exceeding the traditional scope and design of internal accounting functions.

- Risk of late-stage accounting challenges: Transactions are frequently structured by treasury and FP&A teams without sufficient involvement from technical accounting, resulting in unexpected classification and reporting outcomes at period-end.

- In our view there is a need for early technical accounting involvement. Proactive engagement of accounting advisory during the deal structuring phase is critical and should be viewed as a governance necessity rather than an optional step.

- Uniqus supports clients to integrate technical accounting considerations into transaction structuring by collaborating closely with treasury and FP&A teams, enabling upfront identification of accounting implications, avoiding close-period surprises, and strengthening overall financial governance.

Recommended Actions

- Pre-deal accounting impact assessment: Embed technical accounting review as a mandatory gate in the deal structuring process for all financing transactions exceeding a materiality threshold and/or unusual in nature. Assess classification, consolidation, and presentation impacts before signing.

- VIE/consolidation assessment framework: Develop a standardized VIE/consolidation assessment template for SPVs, JVs, and project finance vehicles. Ensure primary beneficiary analysis is documented contemporaneously.

- Embedded derivative screening protocol: Implement a systematic screening process for embedded derivatives in all new financing instruments. Create decision tree for bifurcation analysis under ASC 815-15 and IFRS 9.

- Sale-leaseback pre-assessment checklist: Create a structured checklist for evaluating whether proposed sale-leaseback transactions will achieve sale recognition under ASC 606/842. Flag repurchase options and economic penalties early.

4. Financial Statement Presentation and Disclosure

4.1 Income Statement (P&L) Considerations

Data center costs flow through the P&L in several ways, and the classification choices have significant implications for operating metrics:

- Depreciation expense,

- Energy Cost

- Interest expense

- Impairment charge

To know more, download PDF.

- The depreciation expense classification is a three-way judgment — Cost of Revenue vs. R&D vs. G&A — depending on the function the asset serves.

- For data center companies, the most consequential judgment is the split between cost of revenue (commercial services) and R&D (internal AI research), as this directly affects gross margin and R&D intensity metrics.

- Companies with dual-purpose GPU fleets (serving both commercial customers and internal research) must develop robust cost allocation methodologies, and the allocation percentages should be documented, consistently applied, and disclosed where material.

- In our view, income statement classification for data center costs — depreciation, energy, interest, and impairment — is not a back-office exercise. It is a strategic reporting decision that directly shapes how investors, analysts, and rating agencies perceive operating performance. The three-way depreciation allocation (cost of revenue vs. R&D vs. G&A), the accounting treatment of long-term energy arrangements, the timing of the capitalized-to-expensed interest transition, and the quarterly cadence of impairment trigger monitoring all require coordinated, cross-functional governance that most accounting teams are not currently structured to deliver.

Uniqus supports clients:

- To establish defensible and consistent allocation frameworks for dual-use GPU fleets across commercial and R&D usage.

- To assess PPA structures upfront to determine appropriate accounting under ASC 815, ASC 842, and ASC 606.

- To build phase-level models to track expenditures and anticipate the P&L impact of the “interest cliff.”

- To implement quarterly trigger frameworks aligned with technology cycles and market indicators.

IFRS Perspective:

Depreciation expense

Under IFRS, the same functional classification approach applies — depreciation follows the function of the asset. Under IFRS 18’s new structure, all of these classifications (cost of revenue, R&D, G&A) fall within the operating category, so the mandatory operating profit subtotal captures all data center depreciation regardless of functional line. However, the gross margin impact remains a judgment area for companies that present a gross profit subtotal.

Energy Cost

Under IFRS 18, energy costs associated with revenue-generating operations fall within the operating category. The classification within functional lines (cost of sales vs. administrative) follows the same functional-use principle as US GAAP.

Interest expense

- Capitalization framework: Under IAS 23, capitalization of borrowing costs is mandatory for qualifying assets once construction activities are in progress and expenditures are incurred. This is broadly aligned with U.S. GAAP (ASC 835-20); however, differences may arise in application, particularly regarding the timing of capitalization (commencement, suspension, and cessation) and the treatment of complex, phased data center projects.

- Qualifying asset assessment: IFRS defines qualifying assets as those that require a substantial period of time to be ready for use or sale. While conceptually similar to U.S. GAAP, judgment in interpreting “substantial period” may lead to differences in practice—especially for modular builds, phased commissioning, or rapidly deployable infrastructure common in AI data centers.

- Presentation in financial statements: Under IFRS 18, interest expense is presented within the financing category, separate from operating profit. This creates structural differences in performance reporting compared to U.S. GAAP, where operating income is not formally defined, potentially impacting EBIT and margin comparability across jurisdictions.

Impairment charge

Under IAS 36, the test uses discounted cash flows or fair value less costs of disposal, whichever is higher — a lower threshold that may identify impairments earlier. Additionally, IFRS permits reversal of prior impairment charges (except for goodwill) when conditions improve, while US GAAP does not. This creates a material difference for dual-framework reporters managing GPU fleet transitions where partially obsolete hardware may regain economic utility for inference workloads after an initial impairment for training purposes.

4.2 Balance Sheet Presentation

Data center investments create significant balance sheet complexity across multiple asset and liability categories. The classification and presentation choices carry direct consequences for leverage ratios, covenant compliance, return-on-asset metrics, and investor perception.

IFRS Perspective:

Balance sheet presentation under IFRS is governed by a combination of standards, including IAS 1, IAS 16, IFRS 16, and IAS 37, with a strong emphasis on transparency, disaggregation, and principles-based classification.

Greater disaggregation and transparency:

IFRS, generally require more granular disclosure of asset classes and movements, particularly for PP&E. Data center operators are expected to provide detailed breakdowns of major asset components (e.g., land, buildings, servers, power and cooling infrastructure), along with reconciliation of opening and closing balances, enhancing visibility into capital intensity and asset aging.

Lease accounting impact

Under IFRS 16, all leases (with limited exceptions) are recognized on the balance sheet, resulting in higher reported assets and liabilities compared to U.S. GAAP (which retains operating vs finance lease classification for lessees). This can materially impact leverage ratios, return metrics, and covenant calculations for data center operators with significant lease portfolios.

Construction and capitalization nuances

While the concept of construction in progress (CIP) is similar, IFRS places greater emphasis on continuous capitalization assessment, including borrowing costs under IAS 23 and componentization under IAS 16, which may result in earlier or more granular transfer to depreciable asset categories.

Provisions and AROs

Asset retirement obligations are accounted for as provisions under IAS 37, with discounted measurement and periodic remeasurement. IFRS often require more detailed disclosures of assumptions, timing, and uncertainties, particularly for long-dated environmental obligations typical of data center operations.

Financial instruments and capital structure

IFRS frameworks require careful classification of complex financing instruments, including liability vs equity bifurcation for convertible instruments and fair value treatment of embedded derivatives. Compared to U.S. GAAP, this may lead to greater balance sheet volatility and earlier recognition of equity components.

Consolidation and structured entities

Consolidation under IFRS (control model) may differ in application compared to U.S. GAAP VIE guidance, particularly for SPVs and project financing structures, potentially affecting whether assets and liabilities are presented on-balance sheet.

While the overall balance sheet framework is broadly aligned, IFRS place greater emphasis on disaggregation, full lease recognition, and principles-based classification. For data center investments, these differences can materially alter leverage optics, asset intensity metrics, and comparability across jurisdictions, making early alignment of accounting policies and disclosures critical for global operators.

Recommended Actions

- Policy standardization: Formalize accounting policies for depreciation classification (CoR vs. OpEx), energy costs, and impairment, ensuring consistency across periods and alignment with peer practices.

- Governance framework: Establish a cross-functional Disclosure Committee (Technical Accounting, IR, Legal, Operations) with a defined quarterly cadence to oversee data center–related disclosures.

- Commitment tracking: Implement robust processes to capture and periodically update contractual commitments for data center construction, equipment procurement, and long-term energy arrangements.

- Non-GAAP readiness: Strengthen reconciliation frameworks for non-GAAP metrics (e.g., Adjusted EBITDA, Modified FFO) to align with DISE disaggregation and IFRS 18 MPM requirements.

5. Contingencies and Other Accounting Matters

As data center investments scale at unprecedented speed, organizations are increasingly exposed to non-core but high-impact accounting areas—including contingencies, government incentives, and impairment risks. These elements, while often treated as ancillary, can materially influence financial statements, volatility, and disclosures if not proactively managed.

5.1 Legal and Regulatory Contingencies

The regulatory perimeter around data centres is expanding rapidly—spanning environmental compliance, land-use restrictions, and evolving stakeholder scrutiny. All data center contingencies are assessed under the same accounting framework i.e. ASC 450-

- A loss is accrued when it is probable and the amount is reasonably estimable.

- Where a loss is reasonably possible but does not meet the accrual threshold, disclosure is required.

- What varies across contingency types is not the accounting standard applied, but the practical difficulty of assessing probability and estimation — as outlined below.”

5.2 Tax Incentives and Government Assistance

Governments at federal, state, and local levels are aggressively competing for data center investment through tax incentives—sales tax exemptions on equipment purchases, property tax abatements, investment tax credits, and infrastructure subsidies. Ohio’s data center tax incentive program, for example, has attracted over $10 billion in AWS investment alone. Tax incentives and government support mechanisms are a critical component of data center investment decisions, but introduce nuanced accounting considerations.

IFRS Perspective:

The accounting for contingencies, government incentives, and impairment under IFRS reflects a more principles-based and, in certain areas, more sensitive recognition model.

- Contingencies: Under IAS 37, provisions are recognized when an obligation is more likely than not and can be reliably estimated. Compared to U.S. GAAP, this lower recognition threshold and the use of expected value measurement can result in earlier and potentially higher provisioning.

- Government Grants: IAS 20 provides a well-defined framework for recognition and presentation based on reasonable assurance of compliance with conditions. Entities have clear policy choices between gross (income recognition) and net (asset reduction) presentation, resulting in greater consistency relative to historical U.S. GAAP practice.

Overall, IFRS frameworks tend to drive earlier recognition and greater balance sheet sensitivity, particularly in fast-evolving sectors such as AI infrastructure. For globally operating data center companies, aligning assumptions and ensuring consistency across reporting frameworks is critical to maintaining comparability and transparency.

- Contingencies are becoming strategic, not incidental: In a rapidly evolving regulatory and legal landscape, contingency assessments are no longer periodic compliance exercises but require continuous monitoring and integrated judgment frameworks.

- Government incentives drive economics—but complicate accounting: Tax credits, grants, and subsidies are central to data center investment decisions, yet the absence (historically) of consistent guidance has led to policy fragmentation and disclosure gaps.

- In our view in the AI infrastructure ecosystem, contingencies, incentives, are not peripheral accounting topics—they are strategic levers of financial reporting outcomes. Organizations that embed these areas into core financial governance and decision-making frameworks will be better positioned to manage volatility, enhance transparency, and sustain investor confidence in a capital-intensive, rapidly evolving landscape.

Uniqus supports clients to:

- Build integrated, audit-ready models linking legal, operational, and financial inputs.

- Design standardized policies, tracking mechanisms, and disclosure frameworks related to government incentives.

- Implement proactive impairment frameworks and valuation models.

- Deliver holistic, multi-standard solutions for consistent and decision-useful reporting.

Recommended Actions

- Government incentive tracking system: Build a centralized register of all government incentives, tax credits, abatements, and subsidies. Track compliance with conditions (e.g., green credentials for Virginia). Monitor clawback triggers.

- Incentive accounting policy harmonization: Establish consistent accounting treatment for non-income tax incentives (sales tax exemptions, property tax abatements). Document the analogy to IAS 20 where applied under US GAAP.

- Legal and regulatory contingency assessment process: Establish a quarterly process for assessing legal and regulatory contingencies. Include zoning litigation, environmental penalties, contractual disputes, and IP claims. Document probability and estimation under ASC 450 / IAS 37.

6. DISE (ASU 2024-03) and IFRS 18: Reshaping Presentation

6.1 DISE: Disaggregation of Income Statement Expenses

ASU 2024-03 (codified as ASC 220-40), effective for annual periods beginning after December 15, 2027, for large accelerated filers (December 15, 2028, for all others), requires public companies to disaggregate certain expense line items in the income statement or notes. For data center-intensive companies, the implications are substantial:

What Must Be Disaggregated?

Entities must disaggregate expenses into their natural components—specifically: purchases of inventory, employee compensation, depreciation and amortization, and a residual “other” category. This applies to any line item that contains relevant expense types.

For a data center operator, this means that “cost of revenue”—historically presented as a single large number—will need to be broken out to show the depreciation component (primarily GPU and server depreciation), employee compensation (data center operations staff), energy costs, and other items. Similarly, research and development expense will need to disaggregate depreciation from labor and other costs.

The Data Center Challenge

The practical challenge is significant. Data center costs are typically accumulated in cost centers that blend multiple natural expense categories. Extracting the depreciation component embedded within cost of revenue from the labor and energy components requires system and process changes—new cost allocation routines, subledger configurations, and potentially ERP modifications.

Companies should begin their DISE readiness assessment now, particularly given the system implementation timelines involved. Key steps include mapping current expense flows, identifying data gaps, designing the target-state disaggregation model, and building the internal controls necessary to ensure disaggregated data is complete and accurate.

6.2 IFRS 18: Presentation and Disclosure in Financial Statements

IFRS 18 (effective January 1, 2027) replaces IAS 1 and fundamentally restructures the income statement into five categories: operating, investing, financing, income taxes, and discontinued operations. It also introduces requirements for management-defined performance measures (MPMs).

Impact on Data Center Reporting Under IFRS

For IFRS reporters with significant data center operations, the key changes include:

- Mandatory operating profit subtotal: IFRS 18 defines operating profit as a required subtotal, forcing consistency across reporters. Data center depreciation, energy costs, and operating labor will fall within this subtotal.

- Classification of financing costs: Interest on debt used to finance data center construction, once the asset is placed in service, must be classified within the financing category—not operating. This will reduce the operating profit of heavily leveraged data center operators relative to current practice.

- Management-defined performance measures: Companies that use non-GAAP metrics like “adjusted EBITDA” or “Modified Funds from Operations” (common among data center REITs) will need to provide reconciliations to the nearest IFRS subtotal and maintain consistent definitions year over year.

6.3 Dual-Framework Challenges

Companies reporting under both US GAAP and IFRS face a dual implementation burden. The expense disaggregation requirements of DISE and the income statement restructuring of IFRS 18 are complementary but not identical. Systems and processes must be designed to serve both frameworks simultaneously, particularly for multinational data center operators with entities reporting under different standards.

- Organizations should not defer preparation until the effective date. Given the comparative period requirement, large accelerated filers will need disaggregated data for fiscal year 2027, necessitating that data capture processes are fully operational by January 2027 at the latest. For companies with complex data center operations, the 2026–2027 implementation window is already constrained, making early action critical.

- Uniqus supports clients to navigate these evolving reporting requirements through an integrated approach that combines technical accounting expertise with implementation support.

- We assist in performing DISE impact assessments, designing chart-of-accounts enhancements, and building scalable data architectures that align with both US GAAP and IFRS requirements.

Recommended Actions

- DISE readiness: Conduct a comprehensive impact assessment by mapping expense line items to required natural categories and quantifying embedded components such as depreciation, compensation, and inventory.

- Systems and data architecture: Evaluate ERP capabilities to capture natural expense data; implement necessary chart-of-accounts enhancements, cost center redesign, and automated allocation mechanisms (typically requiring a 6–12 month roadmap).

- IFRS alignment: Assess classification of income and expenses within the IFRS 18 operating category and model the impact of mandatory financing classification of interest on operating profit.

- MPM governance (IFRS): Define Management Performance Measures (MPMs), design reconciliations to IFRS subtotals, and ensure consistency in presentation across reporting periods.

- Dual-reporting strategy: For companies reporting under both US GAAP and IFRS, develop a unified data architecture to support DISE and IFRS 18 requirements, minimizing duplication and enhancing efficiency.

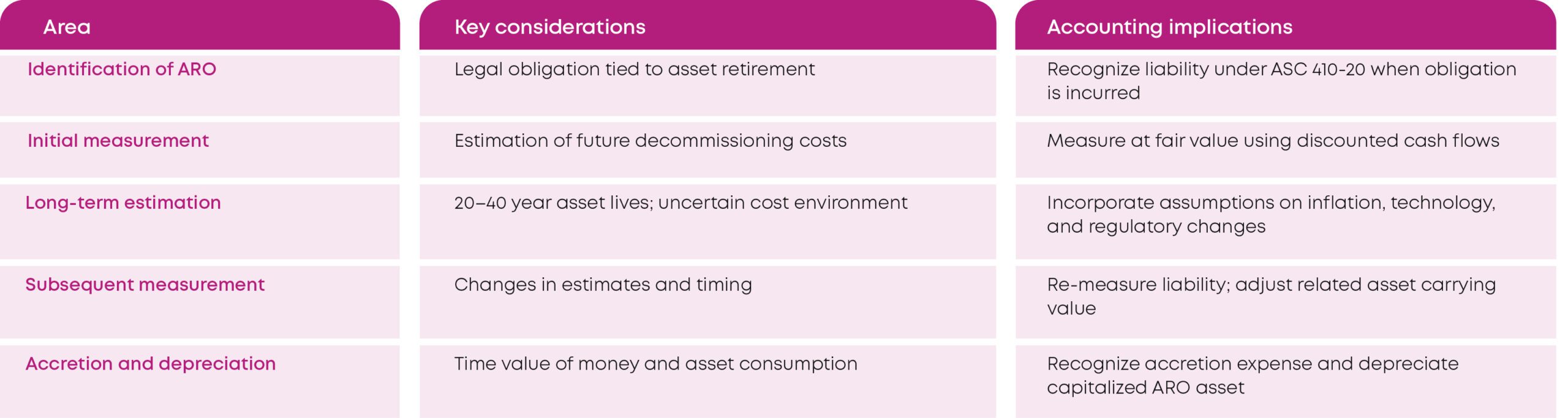

7. Asset Retirement Obligations (AROs)

Data center operations give rise to long-term environmental and decommissioning obligations, including removal of hazardous materials (e.g., batteries, diesel systems, and coolants), site restoration, and disposal of electronic waste. These obligations introduce significant estimation complexity and long-term financial reporting implications. Following summarizes key accounting considerations-

The estimation of ARO amounts for data centers is complex, involving assumptions about decommissioning costs 20–40 years in the future, discount rates, inflation, and the regulatory environment at the time of retirement. These estimates must be revisited periodically and adjusted for changes in expected cash flows or timing.

IFRS Perspective:

Under IAS 37 and IAS 16:

- Decommissioning obligations are recognized as provisions when a present obligation exists.

- The initial estimate is capitalized as part of the asset cost.

- Measurement is based on best estimate, often using discounted cash flows.

- Re-measurements are generally adjusted against the asset (for assets measured under cost model).

In data center environments, AROs are often long-dated but financially significant obligations. The challenge lies not just in estimation, but in maintaining consistency and credibility of assumptions over decades.

In our view Organizations that embed discipline in modeling, governance, and reassessment can better manage both financial statement impact and stakeholder expectations.

Uniqus supports clients in managing ARO complexities through:

- ARO identification and scoping diagnostics across global operations.

- Policy design and documentation frameworks for consistent application.

- Integration with fixed asset and impairment frameworks.

Recommended Actions

- Perform comprehensive ARO scoping assessments across all facilities and jurisdictions

- Develop standardized estimation models for decommissioning costs

- Establish governance over key assumptions (discount rates, inflation, cost inputs)

- Implement periodic reassessment processes aligned with operational and regulatory changes

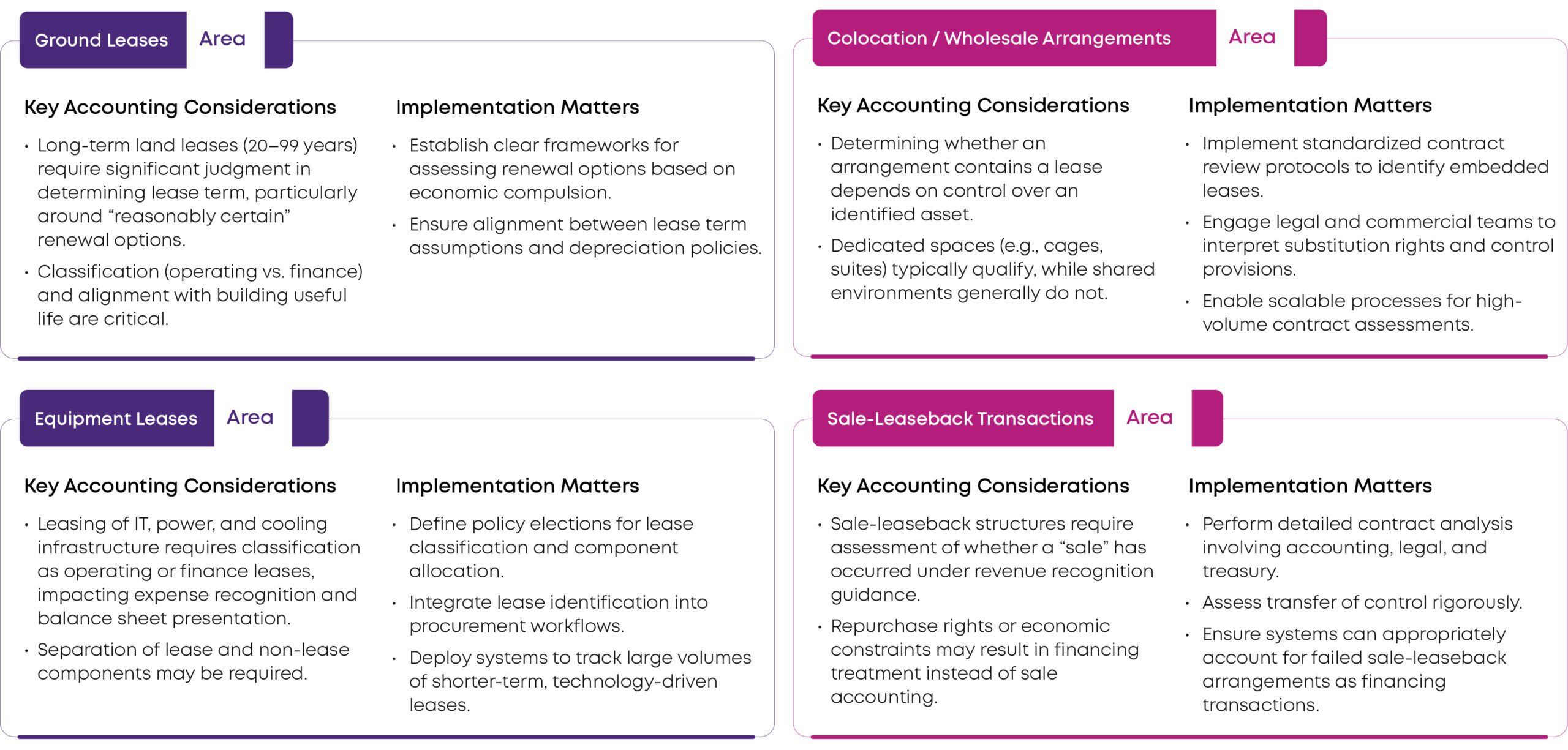

8. Lease Accounting Challenges (ASC 842 / IFRS 16)

Data center business models are inherently lease-intensive, requiring careful evaluation of lease term, classification, and embedded lease considerations across diverse arrangements. The complexity is amplified by long-term contracts, infrastructure dependencies, and evolving commercial structures.

IFRS Perspective:

- IFRS 16 require nearly all leases to be recognized on the balance sheet, eliminating off-balance sheet treatment for operating leases.

- For organizations navigating between US GAAP and IFRS, lease accounting can become a key pressure point—particularly in areas such as embedded lease identification, discount rate determination, and lease term reassessment. A structured, data-driven approach is critical to avoid operational bottlenecks and reporting inconsistencies.

- Lease accounting is no longer a compliance exercise—it is a strategic lever in capital-intensive, AI-driven data center business models.

- As data center investments scale rapidly, lease arrangements are becoming longer-term and more complex. Judgments around lease term, embedded leases, and sale-leaseback structures can significantly influence reported leverage, return metrics, and transaction outcomes.

- In our view organizations that embed discipline in lease accounting early are better positioned to manage investor expectations, optimize deal structuring, and avoid late-stage accounting surprises.

Uniqus supports clients in navigating lease accounting complexities in data center environments through a combination of technical expertise and scalable solutions:

- End-to-end lease diagnostics: Develop comprehensive lease inventories and standardized frameworks for identified asset and lease classification assessments across complex contract portfolios.

- Financial impact modeling: Build dynamic models to quantify the impact of lease accounting on financial statements, KPIs, and debt covenants, including sensitivity analyses.

Recommended Actions

- Comprehensive lease portfolio inventory: Conduct a complete inventory of all data center leases: ground, colocation, equipment, and sale-leaseback. Classify each and document identified-asset, substitution rights, and renewal option assessments.

- Renewal option probability assessment: For ground leases with long renewal options (20–99 years): perform and document reasonably-certain assessment. Align with building depreciation periods and strategic facility plans.

- For planned or contemplated sale-leasebacks: develop a structured checklist covering ASC 606 sale criteria, repurchase options, economic penalties, and leaseback terms. Assess pre-transaction.

Beyond the Hyperscalers: Accounting Challenges for Specialized AI Infrastructure Companies

While much attention is on hyperscalers, a rapidly growing segment of AI infrastructure players operates under fundamentally different financial and accounting dynamics. This includes GPU cloud providers, custom silicon companies, and specialized colocation platforms—building the “middle layer” of AI infrastructure for enterprises and AI labs.

Often venture-backed and capital-constrained, these companies operate in high-growth, high-burn environments where accounting judgments significantly influence financial reporting, investor perception, and access to capital. Their challenges are not simply scaled-down versions of hyperscalers—they are structurally distinct and often more complex.

The accounting challenges these entities face are not merely scaled-down versions of hyperscaler issues. They are structurally distinct—and in several respects, considerably more complex.

Asset-Heavy Business Models Financed with Limited Operating History

The defining characteristic of GPU cloud providers is extreme capital intensity paired with limited operating history. A company might deploy a fleet of tens of thousands of GPUs costing hundreds of millions of dollars—financed substantially through debt—while generating revenue from contracts that may be concentrated among a small number of AI laboratory customers.

The entities operate under highly capital-intensive, debt-funded models with evolving revenue streams and limited operating history. This combination introduces heightened financial reporting complexity, requiring careful judgment across going concern, revenue recognition, and lease accounting.

Going Concern Assessment

- Unlike established hyperscalers, many AI infrastructure companies are scaling rapidly with significant upfront capital deployment (GPUs, data center capacity) supported by leveraged financing structures, while revenue streams remain concentrated and relatively unseasoned.

- For pre-profit or recently profitable companies with significant debt service obligations and capital commitments, the going concern assessment under ASC 205-40 requires management to evaluate whether conditions raise substantial doubt about the entity’s ability to continue as a going concern within one year.

- Management’s plans to mitigate going concern risk through additional equity raises, debt refinancing, cost reduction, or contract diversification must be evaluated for probability under the ASC 205-40 framework. Plans that are not within management’s control (e.g., dependent on future investor appetite) receive limited credit in the assessment.

Revenue Recognition for Compute-as-a-Service

Key aspects of applying ASC 606 for GPU cloud providers include:

- Determining performance obligations and SSPs in hybrid contracts

- Applicability of variable consideration allocation exceptions

- Estimation of variable consideration

- Assessing whether discounts create material rights

- Managing contract modifications and renewals in long-term arrangements

- Ensuring consistent revenue recognition patterns aligned with service delivery

Below are examples of contract structures typically offered with how they fit within the above framework:

- On-demand (pay-per-use): Revenue recognized as services are consumed, by the customer, generally straightforward under ASC 606.

- Reserved capacity (take-or-pay): Customers commit to a fixed amount of compute capacity over a contract term (often 1–3 years), regardless of actual utilization. The accounting question is whether this represents a lease (ASC 842), a service contract (ASC 606), or contains elements of both. If the customer controls the use of specific, identified GPU hardware, the arrangement may contain a lease.

- Pre-paid commitments with volume discounts: Large AI labs may pre-pay for significant compute blocks at discounted rates. Under ASC 606, the entity must evaluate whether the discount constitutes a material right (a separate performance obligation) and whether the pre-payment creates a contract liability.

- Capacity-reservation fees with usage-based billing: Hybrid structures where the customer pays a reservation fee for priority access and then pays variable usage fees. The allocation of the transaction price between the reservation and usage components requires careful analysis of standalone selling prices.

Lease vs. Service Determination

- The distinction between leases and services is a critical accounting judgment with significant implications for both providers and customers.

- If reserved-capacity contracts are determined to contain leases, the provider recognizes lease income (often front-loaded under finance lease treatment) rather than service revenue, and the underlying assets are classified differently on the balance sheet. For the customer, lease classification creates right-of-use assets and lease liabilities that affect leverage ratios and covenant compliance.

IFRS Perspective:

- Under IAS 1 and IAS 36, going concern and impairment assessments may be more sensitive due to principles-based frameworks and discounted cash flow models.

- Revenue recognition under IFRS 15 is largely converged with ASC 606; however, judgment in identifying performance obligations and variable consideration remains critical.

- Lease assessments under IFRS 16 follow a similar control-based model, though lessor accounting differences may impact revenue profiles in certain arrangements.

In our view for specialized AI infrastructure companies, accounting is not just a reporting function—it is integral to business model viability. Decisions around contract structuring, financing, and capacity deployment have direct accounting consequences, making early alignment between finance, legal, and commercial teams essential.

Uniqus supports specialized AI infrastructure companies in navigating these complexities through:

- Going concern and liquidity frameworks aligned with investor and auditor expectations

- Revenue recognition model design, including contract structuring and SSP methodologies

- Lease vs service diagnostics with contract-level analysis and policy standardization

- Integrated accounting advisory, ensuring consistency across CapEx, financing, revenue, and reporting

Recommended Actions

- Establish robust forecasting and liquidity monitoring frameworks to support going concern assessments

- Standardize revenue recognition policies across contract types, including SSP methodologies

- Implement clear lease vs service evaluation frameworks with legal and commercial alignment

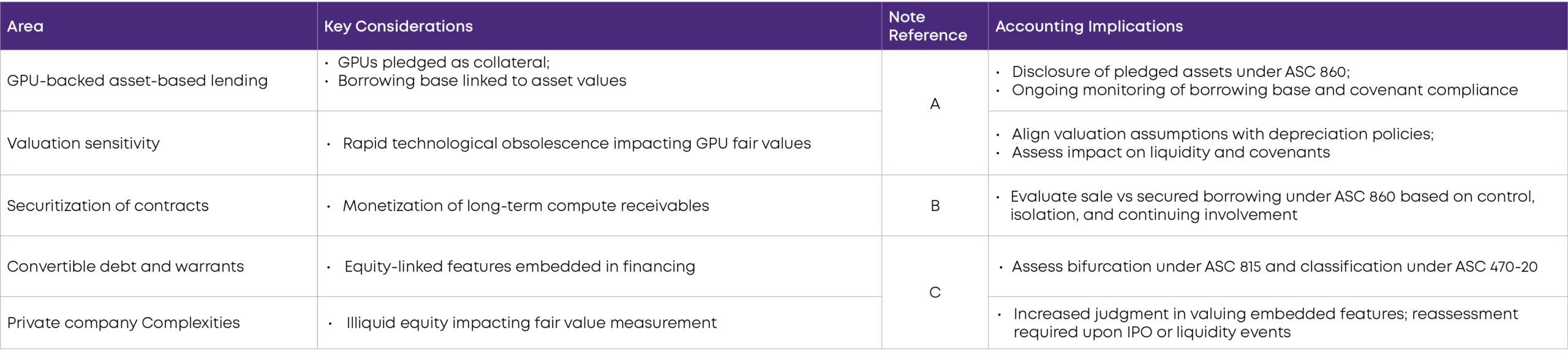

GPU Fleet Financing: Securitization and Structured Debt

To fund large-scale GPU deployments, specialized AI infrastructure companies are increasingly adopting innovative and complex financing structures—including asset-backed lending, securitizations, and equity-linked instruments. While these structures unlock capital efficiency, they introduce significant accounting complexity across financial instruments, transfers, and disclosure frameworks. Following summarizes key accounting considerations:

A. GPU-Backed Asset-Based Lending

Some companies pledge their GPU fleet as collateral for credit facilities, treating GPUs as financeable assets, much like aircraft, shipping containers, or vehicle fleets. The accounting considerations include:

- Collateral pledging disclosures: Under ASC 860 and related guidance, the carrying amounts of pledged assets must be disclosed.

- Covenant compliance: GPU fleet valuations are a key input to borrowing base calculations. Rapid depreciation of GPU values (driven by new chip generations) can erode the borrowing base, triggering covenant violations or margin calls.

- Impairment interconnection: If the borrowing base calculation uses market-based GPU valuations that decline faster than book depreciation, this may also serve as an impairment indicator under ASC 360.

B. Securitization of Revenue Contracts

- Some operators securitize the revenue streams from long-term compute contracts—packaging contracted future cash flows into asset-backed securities (ABS) sold to investors.

- Under ASC 860 (Transfers and Servicing), the key question is whether the transfer qualifies as a sale (with derecognition of the receivables) or a secured borrowing.

- The analysis turns on isolation of transferred assets, the transferor’s continuing involvement, and the transferee’s ability to pledge or exchange the assets.

C. Convertible Debt and Warrant Structures

- Venture-backed AI infrastructure companies frequently raise debt with equity-linked features—convertible notes, warrants, or equity kickers issued to lenders. Under ASC 470-20 and ASC 815, each embedded feature must be evaluated for bifurcation.

- For private companies, the complexity intensifies because the underlying equity is not publicly traded, making fair value measurement of conversion features more judgmental. Companies approaching an IPO must carefully reassess these instruments under public-company GAAP, which can trigger significant remeasurement adjustments in the IPO-period financial statements.

IFRS Perspective:

Under IFRS 9, financial instruments are assessed based on business model and cash flow characteristics, with a strong emphasis on fair value measurement and expected credit loss models.

- Securitization: Derecognition depends on transfer of risks and rewards and control, which may result in earlier or different outcomes compared to U.S. GAAP

- Embedded derivatives: More principles-based bifurcation guidance, often leading to greater use of fair value through profit or loss (FVTPL)

- Disclosures: Enhanced transparency required around risk exposures, liquidity, and financing structures

A new class of AI infrastructure companies is emerging—capital-intensive, leverage-driven, and structurally complex, with balance sheets resembling specialty finance platforms rather than traditional technology firms. However, accounting capabilities often lag this complexity. The resulting gap between financial sophistication and reporting readiness is where the highest risk—and opportunity for value creation—resides.

Uniqus supports AI infrastructure companies in navigating structured financing complexity through:

- End-to-end accounting assessments for securitizations, asset-based lending, and structured debt

- Valuation and modeling support for GPU-backed financing and embedded derivatives

- Covenant monitoring frameworks and stress-testing tools

- IPO readiness advisory, including GAAP conversion and financial instrument re-evaluation

- Integrated advisory across accounting, treasury, and deal structuring, ensuring alignment between financing strategy and financial reporting outcomes

Recommended Actions

- Establish robust valuation frameworks for GPU assets aligned with financing and accounting assumptions

- Implement integrated covenant monitoring tools linking finance, treasury, and accounting

- Perform early-stage accounting analysis for securitization structures to avoid unintended outcomes

- Standardize assessment of embedded features in complex debt instruments

- Prepare for IPO transition impacts, including fair value remeasurements and classification changes

Related Party Transactions and Investor-Customer Overlap

- A distinctive feature of the AI infrastructure ecosystem is the frequent overlap between investors and customers. A venture capital firm or strategic investor may simultaneously hold equity, provide debt financing, and contract for compute capacity. A cloud hyperscaler may be both an investor and the primary customer for a custom chip company’s output.

- These relationships create related party transaction considerations under ASC 850 that require careful disclosure. The concern is whether transactions are conducted on arm’s-length terms.

- Revenue recognized from related parties must be separately disclosed, and the terms of any preferential pricing, guaranteed minimums, or exclusivity arrangements must be transparent.

- For companies preparing for IPO, the SEC staff pays close attention to the substance of related party revenue—particularly where a significant investor is also the dominant customer.

IFRS Perspective:

Under IAS 24, entities are required to disclose:

- The nature of related party relationships,

- Transaction amounts and outstanding balances, and

- Key terms and conditions, including whether transactions are conducted on arm’s-length basis (if asserted).

IFRS frameworks place strong emphasis on transparency and completeness of disclosures, with similar expectations around identifying and presenting related party transactions.

- In the AI infrastructure ecosystem, capital and commerce are increasingly intertwined. While such relationships can accelerate growth, they also introduce heightened scrutiny around revenue quality and transparency.

- In our view, Organizations that proactively address related party considerations through robust governance, clear documentation, and transparent disclosures will be better positioned to withstand regulatory and investor scrutiny.

Uniqus supports clients in managing related party complexities through:

- Related party identification and governance frameworks.

- Arm’s-length benchmarking and documentation support.

- Revenue quality and disclosure diagnostics, particularly for investor-customer overlaps.

Recommended Actions

- Develop centralized related party registers integrated with legal and finance systems.

- Establish policies for evaluating and documenting arm’s-length pricing.

- Enhance disclosure frameworks, particularly for material investor-customer arrangements.

- Conduct periodic reviews of related party transactions to ensure consistency and completeness.

How Uniqus Can Help

Uniqus Consultech brings a differentiated approach to the complex, multi-standard accounting challenges presented by data center investments:

Technical Accounting Advisory

- Capitalization policy design and implementation

- Useful life assessment frameworks

- Complex instrument accounting (convertibles, SPVs, ABS)

- ARO estimation and periodic reassessment

- Lease analysis across ASC 842 / IFRS 16

- Component depreciation model design

DISE & IFRS 18 Readiness

- Gap analysis and impact assessment

- Expense mapping and disaggregation design

- System configuration and ERP advisory

- Internal control design for new data flows

- Dual-framework (US GAAP + IFRS) implementation

- MPM reconciliation design (IFRS 18)

SOX & Internal Controls

- Controls design for capitalization decisions

- Depreciation estimate governance frameworks

- Complex instrument classification controls

- Lease accounting internal controls

- Environmental accrual controls

- DISE data capture and reconciliation controls

Multi-Jurisdictional Reporting

- Tri-framework expertise (US GAAP, IFRS)

- Cross-border DC accounting harmonization