The Supreme Court Ruling: What Happened

The Court’s decision in Learning Resources, Inc. v. Trump resolved a question that had been building since February 2025: whether the President could use IEEPA’s grant of authority to “regulate … importation” as a basis for imposing tariffs. Chief Justice Roberts, writing for the majority, was categorical — the power to regulate importation does not encompass the power to tax imports. IEEPA contains no reference to tariffs or duties, and Congress has consistently used explicit language when delegating tariff authority under other statutes.

The ruling invalidated all tariffs imposed under IEEPA authority, including the reciprocal “Liberation Day” tariffs that applied to most U.S. imports, the fentanyl-related tariffs on Canada, Mexico, and China, and the bilateral tariff arrangements negotiated with several countries. Within hours, the President signed an executive order directing agencies to cease IEEPA tariff collection. However, the majority opinion notably did not address the mechanics of refunds, leaving that question to the lower courts and CBP.

Since the initial ruling, several key developments have occurred, as outlined below:

- On March 4, 2026, the Court of International Trade (CIT) decided in favor of the plaintiff in Atmus Filtration, Inc. v. United States, ordering CBP to liquidate or reliquidate entries without regard to IEEPA duties, effectively directing a refund process for all importers of record.

- On March 6, 2026, CBP filed a declaration requesting a 45-day extension for updates to the automated commercial environment (ACE) system to prepare for the massive volume of refund submissions.

- On March 31, 2026, CBP issued an update reporting significant progress in developing CAPE and that the development of the refund functionality remains on schedule for the mid-April deployment. In addition, the CBP announced that the refunds will be processed in a phased approach, with Phase 1 consisting of unliquidated entries, entries within the 90-day voluntary reliquidation window, and entries with a liquidation status of “Suspended,” “Extended,” or “Under Review.” CBP has estimated that Phase 1 will cover approximately 63% of all entries for which IEEPA duties were paid or deposited, with a go-live target for the CAPE system of April 20, 2026. Once a CAPE Declaration is accepted, CBP expects to process the refund within 45 days, unless a compliance concern requires further review. Finally, liquidated entries (those beyond the 180-day protest window) will not be covered in Phase 1 and are deferred to a subsequent phase with no announced timeline, although the CIT’s March 27, 2026, amended order confirmed that refunds must ultimately extend to those entries as well.

- On April 10, 2026, the CBP issued a bulletin announcing that CAPE would launch the first phase on April 20, 2026. Within the bulletin it also provided instructions on how to request refunds of IEEPA duties.

What Tariffs Remain in Effect?

The SCOTUS ruling only impacts tariffs imposed under IEEPA. The following tariff authorities remain fully intact and are not subject to refund:

- Section 232 tariffs on steel, aluminum, automobiles, auto parts, trucks & buses, copper, timber & lumber, and semiconductors

- Section 301 tariffs on Chinese imports (originally imposed during Trump’s first term)

- Section 122 temporary 10% global tariff (imposed February 24, 2026, post-SCOTUS, 150-day duration)

- Section 201 safeguard tariffs (e.g., solar panels, washing machines)

Companies must carefully distinguish between IEEPA-sourced duties and duties imposed under other authorities when quantifying their refund exposure. Only the former are subject to recovery.

Scale of Impact: The $166 billion in Context

To appreciate the financial reporting challenge, consider the scale. Between February 2025 and January 2026, IEEPA tariff collections followed a steep trajectory, growing from approximately $0.8 billion in February 2025 to nearly $21 billion per month by January 2026. By January 2026, IEEPA tariffs represented more than half of all U.S. customs duties collected. The reciprocal “Liberation Day” tariffs alone accounted for 61% of total IEEPA revenue, with fentanyl tariffs on China contributing 28% and Canada/Mexico tariffs contributing roughly 7%4 .

China bore the highest effective tariff rates at 33.9% by January 2026, reflecting the stacking of IEEPA tariffs on top of existing Section 301 duties. Among product categories, steel and aluminum products faced the highest effective rates at 41.1%, followed by automotive vehicles at 14.9%5 . These rates reshaped supply chain economics for virtually every manufacturer and retailer operating in the United States.

3.1 Sector-by-Sector Exposure Analysis

The IEEPA tariff regime did not impact all industries equally. The following analysis identifies the sectors and highlights the unique accounting challenges each faces.

Sector: Automotive

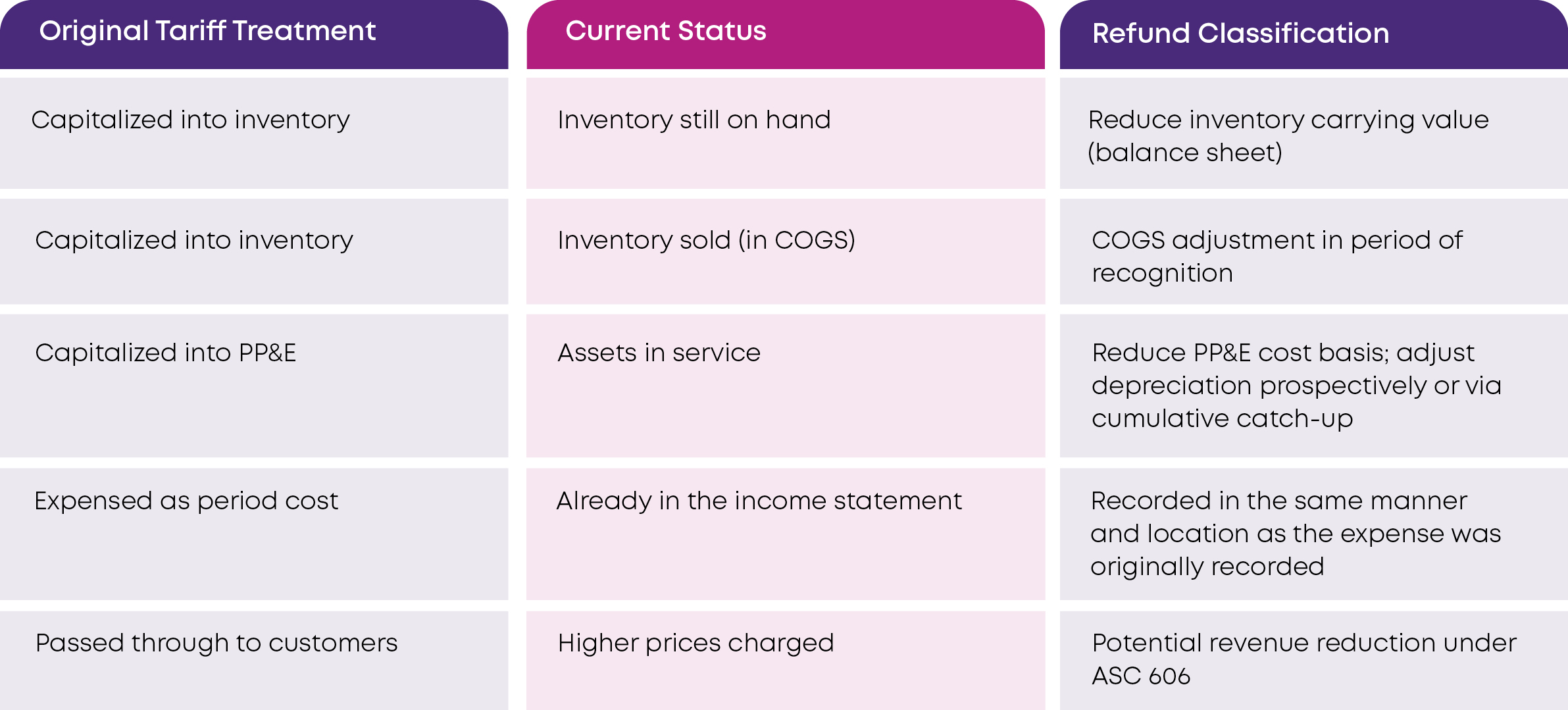

Key Accounting Considerations: Tariffs capitalized into vehicle inventory, PP&E (tooling imported from abroad), and components. Complex supply chains with parts crossing borders multiple times. Refund allocation across finished goods COGS, in-transit inventory, and on-hand inventory is highly judgmental.

Sector: Electronics & Tech Hardware

Key Accounting Considerations: Largest single category of IEEPA-impacted imports (smartphones, computers, components). Rapid inventory turnover means most tariff costs are already in COGS. Refunds are likely to flow primarily to income statement, not balance sheet.

Sector: Pharmaceuticals

Key Accounting Considerations: API (active pharmaceutical ingredients) are heavily sourced from China and India. Tariffs are embedded in manufacturing cost of inventory with long production cycles.Regulatory pricing constraints complicate pass-through analysis.

Sector: Retail & Consumer Goods

Key Accounting Considerations: Thin margins amplify impact. Seasonal inventory cycles mean tariff cost recognition does not align with refund timing. Many retailers passed tariff costs to consumers, creating potential ASC 606 refund obligations.

Sector: Industrials & Chemicals

Key Accounting Considerations: Capital equipment imports and raw materials (resins, specialty chemicals). Tariffs capitalized into PP&E require a prospective depreciation adjustment. Long-lived assets create multi-year unwind complexity.

Sector: Agriculture & Food

Key Accounting Considerations: Imported ingredients, packaging materials, and processing equipment. Highly perishable inventory means tariff costs are already expensed. Government contract pricing provisions may create unique recovery dynamics.

Why are these the primary ASC 606 questions by Archetype:

Automotive: The Most Complex Unwind

The automotive sector arguably faces the most intricate refund accounting challenge. Modern vehicle production involves components crossing borders multiple times — a transmission housing cast in Mexico, machined in the U.S., and assembled into a vehicle with an engine sourced from China. IEEPA tariffs were layered on top of existing Section 232 auto tariffs (25% on finished vehicles), creating stacked duty obligations that must now be disaggregated.

For automotive OEMs, IEEPA tariff costs were typically capitalized into inventory as part of the landed cost of components and finished vehicles. Companies that recognized tariffs as period costs will follow a different refund accounting path than those that capitalized them. The refund, once recognized, must be traced back to the original cost bucket: inventory still on hand receives a carrying value reduction; inventory that has already been sold generates a COGS adjustment.

Electronics: Speed Favors Simplicity

Consumer electronics companies benefit from rapid inventory turns — typically 15–30 days for smartphones and computing hardware. This means nearly all IEEPA tariff costs have already flowed through cost of goods sold by the time refunds are processed. The accounting is relatively straightforward: once the refund is recognized, it appears as a reduction in COGS in the period of recognition. The challenge is scale — a single large hardware company may have billions in refund exposure across thousands of HTS codes.

Pharmaceuticals: The API Supply Chain Problem

Pharmaceutical companies face a unique challenge because their tariff exposure is concentrated in active pharmaceutical ingredients (APIs) and chemical intermediates, many of which are sourced from China and India. These inputs have long production cycles — the inventory produced with tariff-burdened APIs may still be sitting in warehouses, in distribution, or partially consumed. Reconstructing which finished drug inventory items carry IEEPA tariff costs and which carry Section 301 or other tariff costs requires granular, lot-level traceability that many companies’ ERP systems were not designed to provide.

Retail: The Consumer Pass-Through Dilemma

Retail companies that passed tariff costs through to consumers face a distinct question under ASC 606 (Revenue from Contracts with Customers). If a retailer received a tariff refund on goods for which it charged customers a higher price to offset tariffs, does the refund create an implied refund obligation to customers? The answer depends on the contractual terms, pricing representations, and commercial practice. Companies that explicitly represented tariff surcharges as pass-through items may find that the refund reduces their transaction price, effectively treating the refund as a revenue reduction rather than a cost recovery.

US GAAP Accounting Framework

As a direct result of this overruling, there are two potential financial implications: 1) Potential Refunds from CBP for IEEPA tariffs and 2) Potential refunds to Customers for Tariffs. There is no explicit US GAAP guidance on accounting for tariff refunds when the underlying tariff is judicially invalidated. This is not a gap the FASB anticipated. In the absence of direct guidance, companies and their auditors must choose between two established frameworks, each with a different recognition threshold and potentially different income recognition timing.

4.1 Possible IEEPA tariff refunds

When determining whether an asset should be recognized related to future refunds on previously paid IEEPA tariffs, one of two models can be applied:

- Loss Recovery Model under ASC 410-30 (Model A); or

- Gain Contingency Model under ASC 450-30 (Model B)

Loss Recovery Model (Model A)

In order for a loss recovery model to be applicable, a company would have had to incur a loss as a result of the IEEPA tariffs. We believe in situations where a company has passed on the IEEPA tariffs to the end-customer, this position may be difficult to support.

Under the loss recovery model:

- An asset for the tariff refund claim is recognized when recovery is probable (i.e., likely to occur). The classification between current vs. noncurrent should be based on the expected period of settlement.

- The amount of refund claim recognized as an asset is limited to the loss amount.

- Any potential recovery above the loss would need to be treated under the gain contingency model.

- The recovery is not netted against the original loss; it is recognized as a separate line item, typically as a reduction in cost of goods sold.

Key Advantage of Model A

The loss recovery model permits earlier recognition than the gain contingency model. To the extent that the government’s ability to appeal the latest order lapses on June 6, 2026, and the companies have strong legal positions, have filed protests with CBP, and can point to favorable CIT orders, this model may allow balance sheet recognition in 2026 potentially as early as Q2.

Gain Contingency Model

Under the gain contingency model:

- A gain contingency is not recognized in the financial statements until it is realized (i.e., cash received, or amount fixed and determinable with certainty).

- Gain contingencies cannot be recognized based on expectation, likelihood, or public announcements — even a Supreme Court ruling that the tariffs are unlawful.

- The only acceptable treatment before realization is disclosure in the footnotes, provided the contingency is material.

Key Advantage of Model B

Under this model, no asset appears on the balance sheet until CBP has formally processed and approved the specific refund. Although the recent CBP guidance on entries falling under the Phase 1 categories has shed light on the rollout of CAPE, it is not yet complete, and uncertainty remains. Further, entries that do not fit the Phase 1 categories remain uncertain regarding timing. As the “realized” is likely not met, this model may defer recognition until after Q2 2026 for Phase 1, and potentially later for entries not meeting Phase 1.

Depending on the model utilized, companies must apply it consistently to all IEEPA tariff refund claims. The accounting model applied should clearly be documented, disclosed in the footnotes, and discussed with the external auditor early in the process.

4.2 Payments to Customers

Depending on the contractual terms, pricing representations, and commercial practice, a company may be required to refund tariff costs paid by customers. Any refunds paid to customers should be analyzed as consideration payable to customers under ASC 606. To the extent such consideration payable to a customer is not a payment for a distinct good or service, the payments should be accounted for as a reduction of the transaction price at the later of the following:

- A company recognizes revenue for the transfer of the related goods or services; or

- A company pays or promises to pay the consideration.

4.3 Subsequent Event Analysis (ASC 855)

For December 31, 2025 year-end filers, the SCOTUS ruling on February 20, 2026 is a subsequent event that must be evaluated under ASC 855. The central question: is the ruling a Type 1 (recognized) or Type 2 (non-recognized) event?

The prevailing view among national firms is that the SCOTUS ruling is a Type 2 non-recognized subsequent event. The rationale: while the underlying constitutional limitation may have always existed, the tariffs were legally enforceable obligations that companies were required to pay until the Court ruled otherwise. The ruling represents a change in the law, not evidence of a condition that existed as of December 31, 2025. This means December 31 financial statements should not be adjusted, but robust footnote disclosure is required.

Companies electing the loss recovery model should note that changes in probability after the balance sheet date — such as favorable CIT orders in April/May 2026 — could be relevant to the subsequent events assessment and may need to be considered through the financial statement issuance date.

4.4 Where Does the Refund Land in the Financial Statements?

The financial statement classification of a tariff refund depends on where the original tariff cost was recognized:

The accounting for IEEPA tariff refunds is further complicated by income tax and transfer pricing implications that require coordination between tax and financial reporting teams. Companies should hold early discussions with their tax team/experts to ensure proper consideration is being given to the impacts to their tax positions as a result of the IEEPA tariff refunds.

IFRS Considerations: Where the Standards Diverge

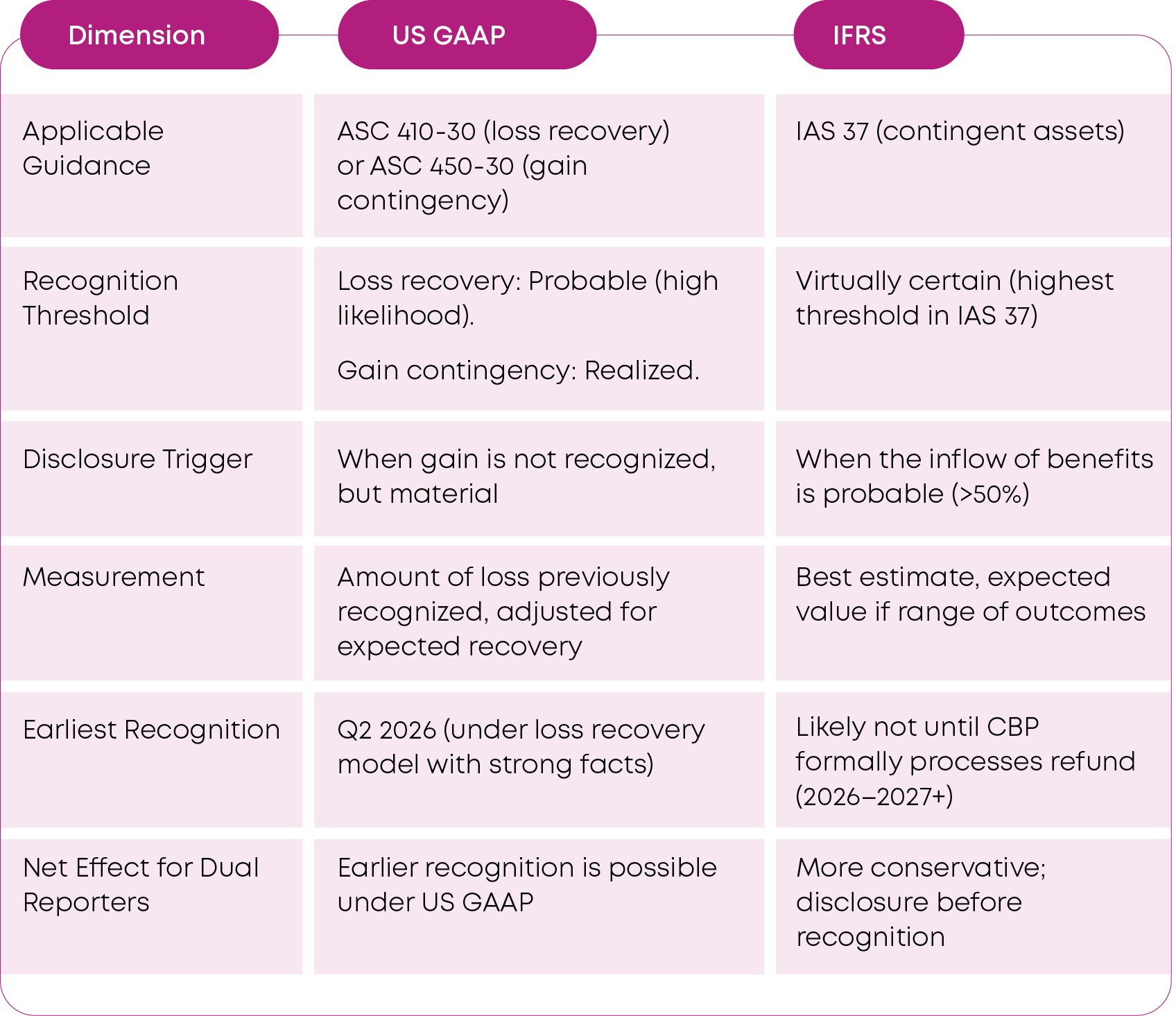

For multinational companies reporting under IFRS, or U.S. companies with IFRS-reporting subsidiaries, the accounting for IEEPA tariff refunds introduces a different set of considerations under IAS 37 (Provisions, Contingent Liabilities and Contingent Assets). While the broad principles are similar, there are meaningful differences in recognition thresholds and measurement that could lead to divergent outcomes between US GAAP and IFRS financial statements.

5.1 Contingent Assets Under IAS 37

Similar to US GAAP, the SCOTUS ruling on February 20, 2026 is a subsequent event that must be evaluated under IAS 37. The central question: is the ruling a Type 1 (recognized) or Type 2 (non-recognized) event?

Not probable: (possible but not more likely than not): No recognition, no disclosure required unless material.

Probable: (more likely than not, i.e., >50% likelihood): Not recognized but disclosed in the notes with an estimate of financial effect if practicable.

Virtually certain: The asset is recognized in the financial statements. At this point, IAS 37 says the asset is no longer “contingent.”

Critical IFRS vs. US GAAP Difference

Under IFRS, “probable” means >50% likelihood — a lower threshold than US GAAP’s interpretation of probable as “high likelihood.” However, IAS 37 only allows recognition of a contingent asset when it is “virtually certain” — a higher threshold than the ASC 410-30 loss recovery model’s “probable” recognition trigger.

Net effect: IFRS reporters may reach the disclosure threshold sooner, but the recognition threshold is later than that of US GAAP reporters using the loss recovery model.

5.2 The Reimbursement Asset Model Under IAS 37

IAS 37.53–58 provides guidance on reimbursement assets that is relevant by analogy. When an entity expects to be reimbursed for an expenditure required to settle a provision, the reimbursement is recognized as a separate asset only when it is virtually certain that the reimbursement will be received. The reimbursement asset cannot exceed the amount of the provision.

The tariff refund situation is not a direct provision or reimbursement, but the principle is instructive: IFRS requires a very high degree of certainty before an asset can be recognized for expected recoveries. Given the current uncertainties around the CBP refund process, the administration’s resistance, and the absence of entity-specific refund approvals, it is unlikely that most companies could conclude “virtual certainty” exists as of Q1 2026 under IFRS.

5.3 Comparative Summary: US GAAP vs. IFRS

For dual-reporting entities, this divergence creates a practical challenge: the US GAAP financial statements could show a refund receivable on the balance sheet while the IFRS financial statements show only a footnote disclosure.

5.4 Events After the Reporting Period (IAS 10)

IAS 10 (Events After the Reporting Period) draws the same distinction as ASC 855 between adjusting events (conditions existing at balance sheet date) and non-adjusting events (conditions arising after). For December 31, 2025, IFRS financial statements, the analysis parallels the US GAAP conclusion: the SCOTUS ruling is most likely a non-adjusting event that requires only disclosure.

Internal Controls and SOX Implications

With the potential for the IEEPA tariff refund to have a significant impact on a company’s financial statements, controls become a relevant consideration, especially for SEC registrants subject to SOX 404. The complexity and materiality of tariff refund accounting demand a deliberate internal controls response.

Areas Requiring New or Modified Controls

Data completeness and accuracy: Controls over the completeness of the IEEPA tariff refund population, including reconciliation of customs broker data to the general ledger, identification of liquidated vs. unliquidated entries, and separation of IEEPA duties from Section 232/301 duties.

Accounting model application: A management review control (MRC) over the selection and documentation of the accounting model (loss recovery vs. gain contingency).

Probability assessment: Controls over the initial assessment of probability as well as ongoing reassessment as new facts emerge (CIT orders, CBP processing updates, litigation outcomes). This is an estimate that will evolve quarter-to-quarter and requires a well-documented, evidence-based judgment.

Classification and measurement: Controls over the proper classification of refunds across inventory, COGS, PP&E, and/or revenue — including the ASC 606 pass-through analysis for retailers.

Disclosure review: Management review control over the completeness, accuracy, and compliance of tariff refund disclosures in Forms 10-K and 10-Q.

Coordination with trade counsel: Controls ensuring that the accounting team receives timely updates from legal and trade compliance on CBP protest status, litigation developments, and refund processing.

SOX Consideration

Failure to design and implement appropriate controls over IEEPA tariff refund accounting could itself become a control deficiency. If the amounts are material and the controls are absent or ineffective, this could escalate to a significant deficiency or, in severe cases, a material weakness — particularly if it results in a material misstatement in the tariff refund receivable or related disclosures.

The Uniqus Perspective

At Uniqus, we believe this is a once-in-a-generation accounting event — and it demands more than a check-the-box response from controllership teams. Below is Uniqus’ view on the critical judgment calls.

On the Accounting Model: Probability-Assessment

If a company plans to apply the loss recovery model (ASC 410-30 by analogy), a thorough review of the fact patterns and company-specific considerations should be conducted when performing the probability assessment. Consistent with the updates issued by the CBP on March 31, 2026, the refund process will follow a phased approach, with Phase 1 being the first phase subject to refund upon deployment of the CAPE system. By bifurcating the total refund population into entries subject to Phase 1 vs. entries subject to later phases, this approach will help support the probability, as the hurdle to assess the “probable” threshold for Phase 1 entries may be easier to overcome than for entries that would not be covered under Phase 1.

On Disclosure: Go Deep, Go Early

Regardless of which model is elected, the disclosures must be comprehensive. We recommend that companies disclose: the accounting model elected and the rationale; the aggregate IEEPA tariff exposure by financial statement line item (inventory, COGS, PP&E); the status of CBP protests and any litigation; the key assumptions underlying the probability assessment; the estimated range of refund amounts (if determinable); and any remaining uncertainties that could affect timing or amount of recovery. To the extent the impacts are expected to be material, investors and analysts may expect discussion in SEC filings regarding expected earnings impact and the timing sensitivity.

On Cross-Border Implications: Think Holistically

For multinational groups, the divergence between US GAAP and IFRS recognition creates a real reconciliation challenge. We advise dual-reporting entities to align their disclosure strategies, even if recognition timing differs—ensure that the narrative in both sets of financial statements tells a consistent story, and that the reconciliation between US GAAP and IFRS explicitly addresses the timing difference in the tariff refund.

CFO and Controller Action Checklist

Based on our analysis, the following actions should be prioritized in the next 30–90 days:

- Build the refund inventory: Reconstruct all IEEPA tariff payments by customs entry, HTS code, country of origin, payment date, and liquidation status. Reconcile to the general ledger. Separate IEEPA from Section 232/301 duties.

- Elect and document your accounting model: Prepare a formal accounting policy memorandum selecting either the loss recovery model or the gain contingency model. Document the rationale and discuss with external auditors.

- Perform the probability assessment: If you use the loss recovery model, prepare a detailed memorandum evaluating the probability as of each reporting date. Include legal opinions, CIT order analysis, CBP processing status, and entity-specific filing history.

- Engage trade counsel immediately: Ensure timely filing of CBP protests on liquidated entries. Evaluate whether to join protective CIT lawsuits. The accounting team cannot assess probability without legal input.

- Trace the refund to financial statement line items: Map each tariff payment to its current financial statement location (inventory, COGS, PP&E, period expense). This determines where the refund credit will land.

- Evaluate ASC 606 implications: If your company passes tariff costs through to customers, assess whether the refund creates an implied refund obligation or a variable consideration adjustment under revenue recognition guidance.

- Design internal controls: Implement controls over refund data completeness, probability assessment updates, classification accuracy, and disclosure compliance. Document in the RCM and communicate with the external auditor.

- Coordinate with tax: Align the financial reporting treatment with the income tax treatment including transfer pricing implications. Involvement of tax experts is required.

- Prepare comprehensive disclosures: Draft footnote disclosures covering the accounting policy, exposure amounts, probability assessment, key uncertainties, and expected timing. Update MD&A, risk factors, and earnings guidance as appropriate.

- Brief the audit committee: This is a critical accounting estimate that requires audit committee awareness and, in many cases, approval of the accounting model election. Prepare a concise briefing covering the decision framework, magnitude, and earnings sensitivity.

Looking Ahead: What to Watch

The IEEPA tariff refund story will evolve over the coming quarters. CFOs should monitor:

- CBP refund processing: Whether CBP establishes a formal administrative mechanism for refunds, or whether individual court orders remain the primary enforcement tool.

- CIT rulings: The Court of International Trade is actively managing multiple cases; its orders on scope, procedure, and interest calculations will shape the refund landscape.

- Administration response: Whether the executive branch appeals, resists, or cooperates with refund processing. The President has signaled resistance, but Treasury Secretary Bessent has previously acknowledged that invalidation requires refunds.

- Congressional action: Whether Congress legislates a refund mechanism or attempts to impose conditions on repayment. Section 122 tariffs expire on July 24, 2026, unless extended.

- FASB or SEC guidance: Whether the FASB or SEC staff issues interpretive guidance or an SAB addressing the tariff refund accounting framework. The current vacuum of explicit guidance creates an opportunity for standard-setters to provide clarity.

- Peer company disclosures: As Form 10-Q filings for Q1 2026 emerge in May–June, companies will benchmark their disclosures and accounting model elections against industry peers.