Introduction

The Indian insurance sector has long operated under a financial reporting framework shaped by the Insurance Act, 1938, a framework designed primarily to support prudential oversight and policyholder protection, rather than to serve the informational needs of a globally connected investor base. While this framework has served its purpose well, the evolving dynamics of global capital markets, increasing foreign investment in Indian insurance companies, and the widespread international adoption of IFRS 17 have made a structured transition to Ind AS both relevant and necessary.

Ind AS, which is substantially converged with IFRS, has already been implemented across most of India’s corporate sector. Banks and Non-Banking Financial Companies (NBFCs) have been reporting under Ind AS since 2018-19. The insurance sector was the remaining significant exception, and the IRDAI’s March 2026 Exposure Draft closes that gap decisively.

The proposed implementation is uniform: all insurers, regardless of size, listing status, or business mix, shall adopt Ind AS from 1st April 2026. During the first year, insurers will be required to submit both Ind AS financial statements (statutory reporting) and Indian GAAP-based financial information (special-purpose regulatory submission) in parallel, enabling a rigorous impact assessment of the transition.

The key concepts introduced under Ind AS that will fundamentally alter insurance accounting in India are:

Ind AS 117 (Insurance Contracts): A comprehensive, principle-based framework for recognition, measurement, presentation, and disclosure of insurance contracts, introducing measurement models such as the General Measurement Model (GMM), Premium Allocation Approach (PAA), and Variable Fee Approach (VFA)

Ind AS 109 (Financial Instruments): Governing the classification, measurement, and impairment of financial assets and liabilities, including the forward-looking Expected Credit Loss (ECL) model

Ind AS 1 (Presentation of Financial Statements): Prescribing the overall structure and minimum content of financial statements

Ind AS 113 (Fair Value Measurement): Providing the framework for fair value determination across asset and liability classes

This Early Impressions piece outlines the key assessment areas, proposed regulatory solutions to critical policy choices, and a practical implementation agenda for insurers, CFOs, and Boards navigating this transition.

What Does It Mean for Insurers?

A Fundamental Shift in How Profit is Measured and Reported

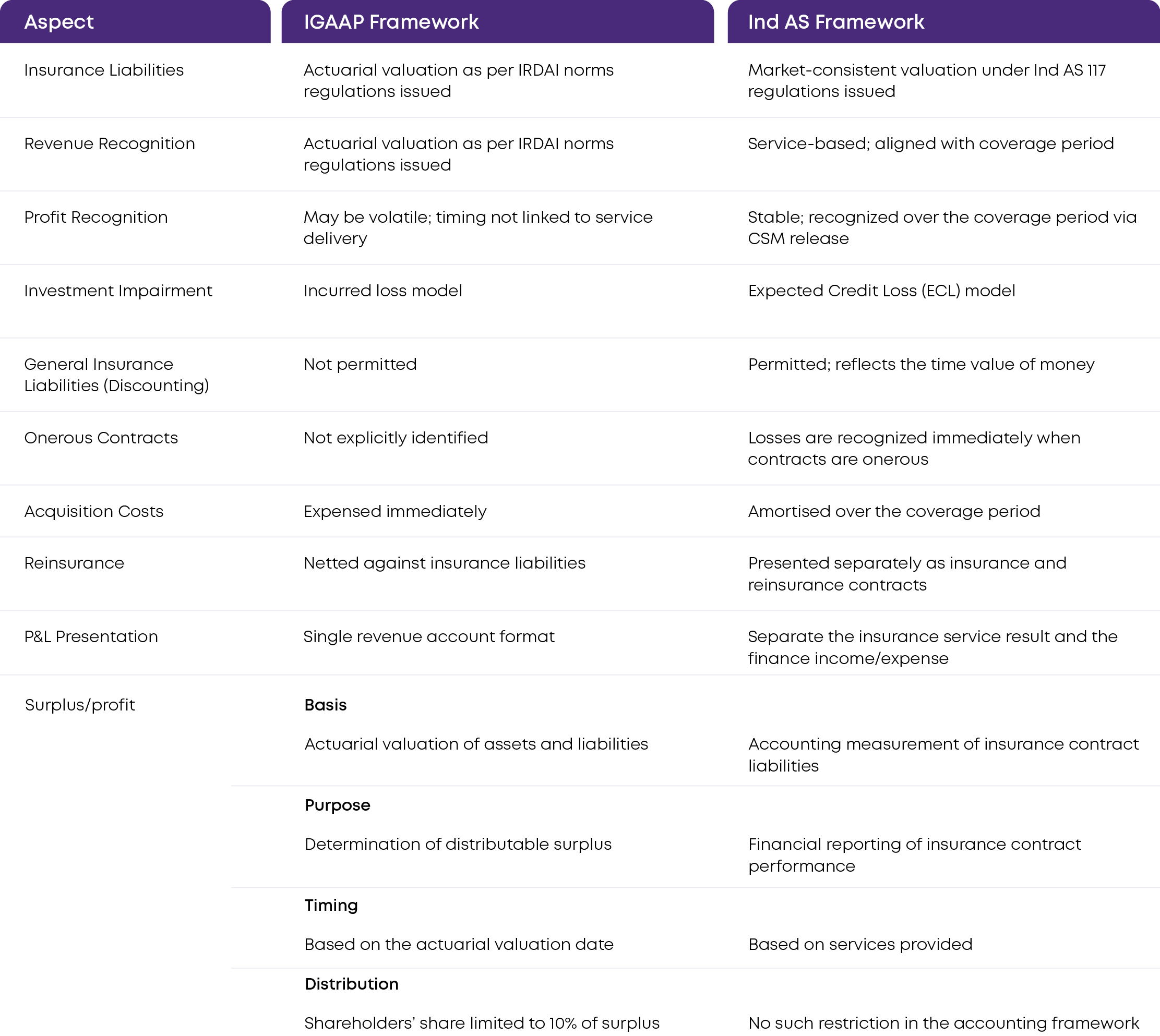

The transition from IGAAP to Ind AS is not an incremental update. It is a structural change in the economics of financial reporting. The table below summarises the most significant differences:

The Regulatory Catalyst: Why April 2026?

The IRDAI’s decision to mandate full adoption from 1st April 2026 reflects both the global imperative and the industry’s demonstrated preparedness. Globally, IFRS 17 has been effective since 1st January 2023 across major jurisdictions, including the European Union, Australia, Canada, Singapore, Malaysia, Hong Kong, South Africa, and the UAE. India’s delayed adoption has increasingly positioned Indian insurers as outliers in an otherwise converged global reporting landscape, constraining comparability with international peers and limiting the attractiveness of Indian insurance companies to foreign institutional investors.

The timing may also reflect a compelling domestic catalyst. The Sabka Bima Sabki Raksha (Amendment of Insurance Laws) Act, 2025, now permits foreign investment in Indian insurance companies up to 100% of the paid-up equity capital. Non-IFRS financial statements represent a material barrier to unlocking this investment potential. Ind AS adoption directly addresses this by providing globally comparable, transparent financial reporting that international investors can benchmark and rely upon.

Key Assessment Areas

1. Ind AS 117: The New Architecture of Insurance Accounting

What is changing?

Under the existing IGAAP framework, insurance liabilities are measured using actuarial valuation norms prescribed by IRDAI. These valuations are primarily designed to support solvency monitoring and policyholder protection, not to reflect current market-consistent economic assumptions. As a result, profit patterns under IGAAP often do not clearly reflect the economic performance of insurance contracts, and the reported financial position may diverge materially from economic reality.

Ind AS 117 replaces this with a comprehensive, current-value measurement framework built on three measurement models:

Three concepts in particular will require significant recalibration of systems, actuarial processes, and finance functions:

A. Fulfillment Cash Flows

Under Ind AS 117, insurers must estimate probability-weighted, discounted future cash flows, encompassing future premiums, claims, expenses, and acquisition costs, updated at every reporting date. These estimates are no longer anchored in historical assumptions; they reflect current best estimates and include an explicit risk adjustment for non-financial risk. This represents a fundamentally different approach to liability valuation from the actuarial norms currently prescribed under IRDAI regulations.