Background and Changes Proposed

The RBI has been actively implementing new guidelines to make certain that the Indian banking industry continues to be resilient and competitive on the global stage while also being robust financially. The Reserve Bank issued a draft circular on July 25, 2024, on ‘Basel III Framework on Liquidity Standards – LCR – Review of Haircuts on HQLA ‘ and Run-off Rates on Certain Categories of Deposits. The draft circular proposed certain amendments to the LCR framework and invited comments from banks and stakeholders.

Following this and the industry consultation, the RBI has finalized the amendments to the LCR framework. The following are the changes proposed:

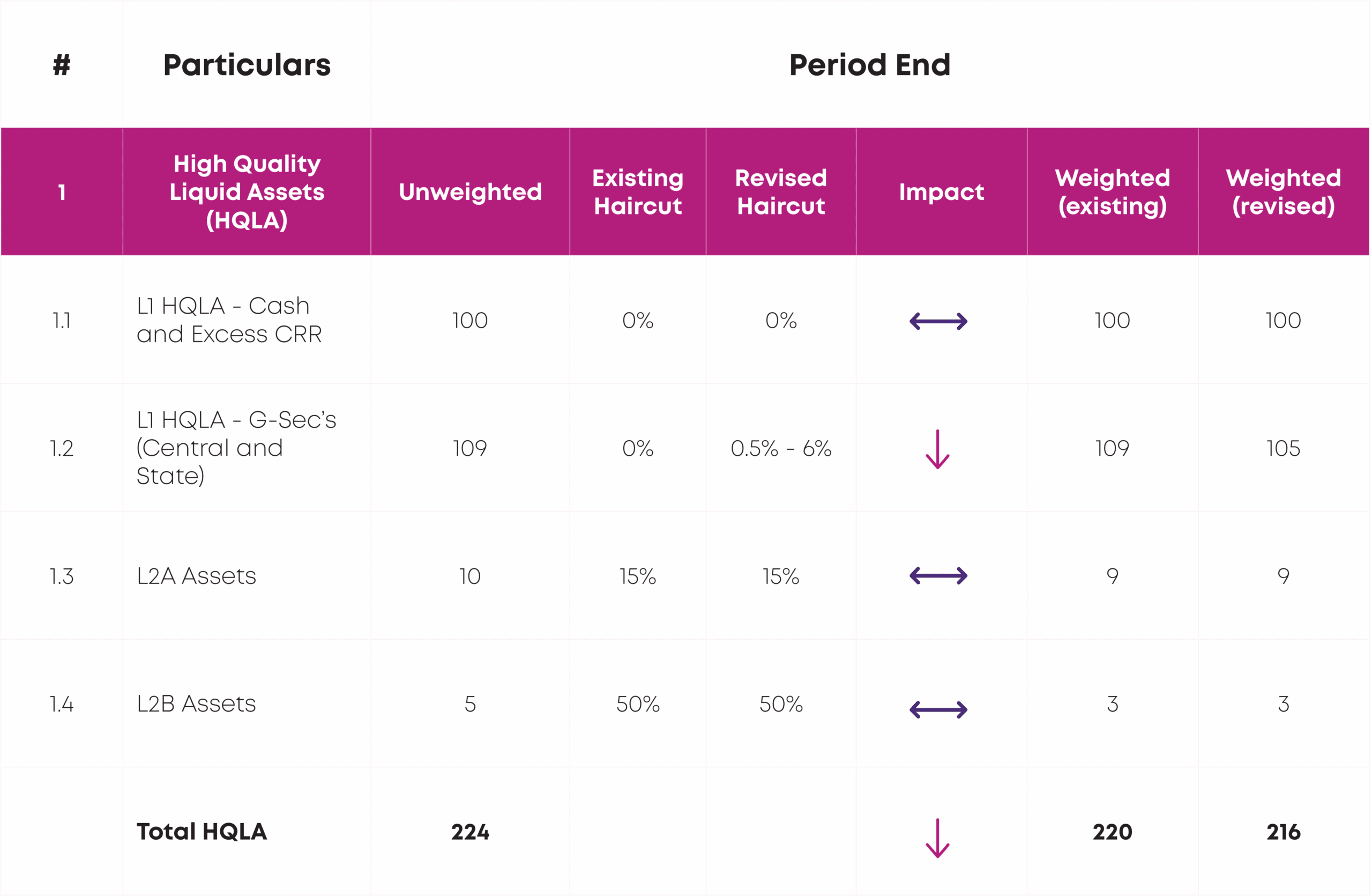

- Adjust the market value of the G-Sec’s (Central and State) in the LCR using the applicable haircut as per margin requirements under LAF/MSF norms. As a result, haircuts on G-Sec’s under L1 Assets will range from 0.5% to 6%, depending on the category of the instrument (Central or State) and residual maturity.

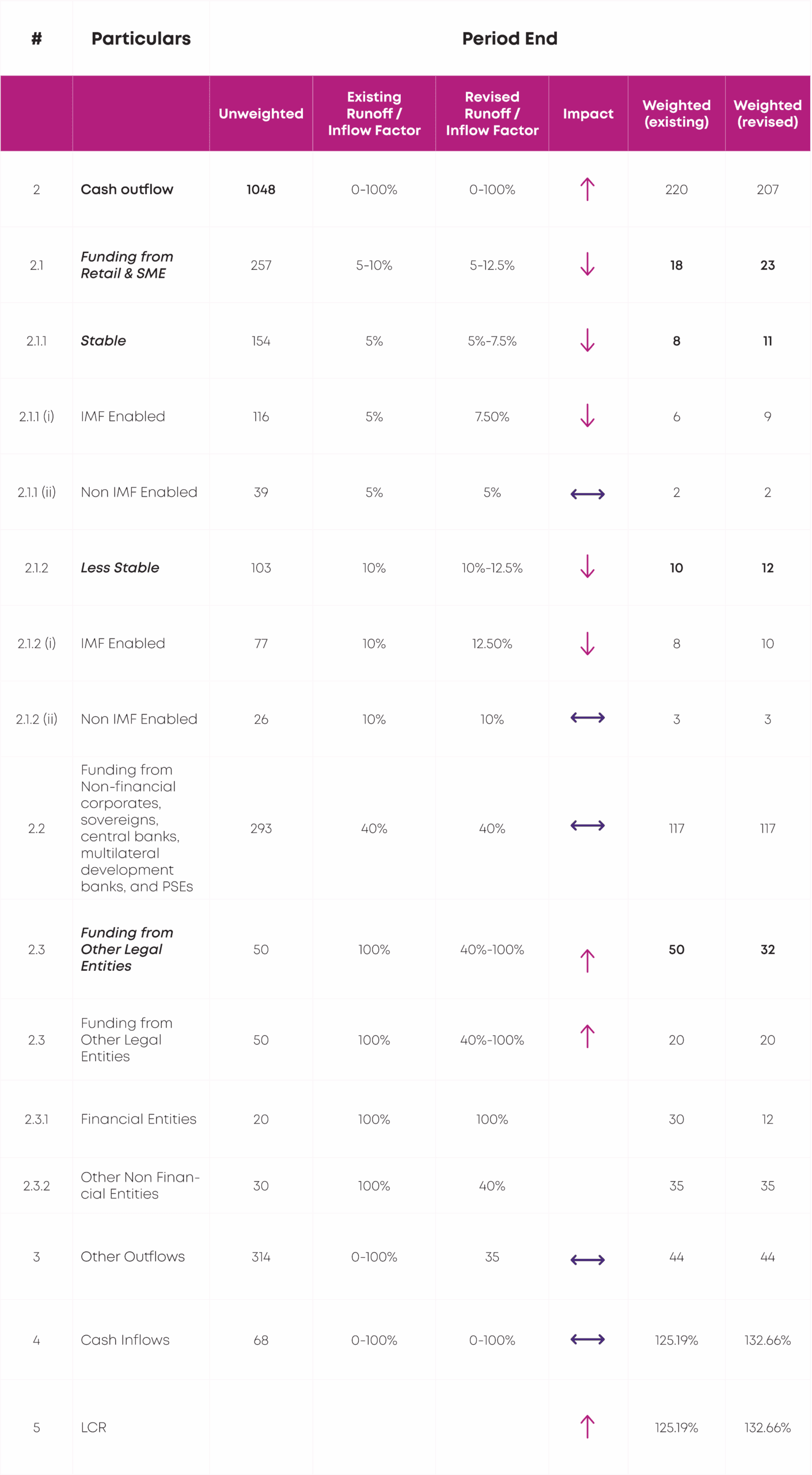

- An increased run-off factor (additional 2.5%) will be applied to deposits raised from Retail and Small Business customers with activated internet and mobile banking.

- Deposits currently classified as ‘Other Legal Entities’ (including financial institutions, trusts, and partnership firms) and subject to a 100% run-off factor should now be further bifurcated into Financial and Non-Financial entities. Non-financial entities will now be eligible for a reduced 40% run-off factor.

These changes are proposed with a view to bolstering the LCR framework in response to the following:

- The current market value of G-Sec’s may not be fully realizable during periods of stress, and hence, haircuts have been aligned with margin requirements.

- The growing pace of digital adoption has increased the speed at which customers can withdraw or move funds during stress, posing liquidity risk to the banks.

- Carving out Non-financial entities from Other legal entities helps reduce the ongoing ambiguity on customer classification and keeps other legal entities for entities closely linked to the financial ecosystem.

While the first two changes proposed will have a downward impact on the LCR, the third change is expected to offset this by lowering outflow on account of wholesale funding from non-financial entities. As a result, the net effect on the LCR is expected to be positive.

Key Impact

While LCR has been in effect for more than a decade now, amendments have been made from time to time to reflect the actual risk and accordingly adjust the HQLA requirements. Changes proposed in the current framework will have an impact on various components of liquidity risk and overall balance sheet management.

The following is the quantitative impact on the LCR due to the changes proposed:

Based on the following assumptions, we see the net positive impact of ~7.5% on the LCR:

G-Sec Haircuts: A flat haircut of 4% has been applied on all Central and State Government Securities, instead of using variable haircuts based on residual maturity.

Outflow Composition: Total outflows have been split into three categories:

- 35% from Retail & SME deposits

- 35% from Non-Financial Corporates

- 30% from Other Legal Entities

Operational Deposits: Assumed to be nil, i.e., no favorable treatment applied.

IMB-Enabled Deposits (Retail & SME): Assumed that 75% of Retail and SME customers are digitally active, based on data from various banks.

Financial Entity Funding: Assumed that 40% of deposits under the ‘Other Legal Entities’ category are from financial institutions.

Cash Inflows: The Inflow factor on cash inflows has been considered at 65%, based on a review of inflow patterns across select sample banks.

Apart from the impact on LCR, there will be a ripple impact on other critical areas due to the changes proposed, which are categorized broadly into three themes – Funding Strategy, Profitability, and Balance Sheet Optimization:

A. Funding Strategy

- Shift in focus in terms of digital offerings to retail and SME customers – with higher run-offs for customers who are IMB-enabled, banks need to re-evaluate the acquisition strategy and accordingly price in the same.

- Diversification in wholesale funding – The reduced run-off for certain non-financial entities (trusts, LLP, professional bodies) makes them more attractive from an acquisition standpoint. Banks may need to incentivize the business managers via FTP to acquire these customers.

- Funding Cost: Evaluate the funding cost due to change in the mix and accordingly price in benchmark rates and risk-based pricing.

B. Profitability

- Durable liquidity release – Net liquidity release through changes proposed can be redeployed into higher-yielding assets (maintaining the same level of LCR).

- FTP adjustments will impact pricing across product, business unit and customer level.

C. Balance Sheet Optimization

- HQLA portfolio rebalancing – Actively manage the G-Sec’s portfolio by issuer type and maturity profile to optimize the LCR and funding cost.

- Risk Models – Changes will flow into internal stress testing, ICAAP assessments, and strategic liquidity buffers, requiring calibration of model assumptions and scenarios.

Key Actionable Themes for the Banks

To ensure seamless adoption of the proposed changes, banks will need to take a structured implementation approach over the one-year transition period. The following are the actionables bifurcated into – Operational execution and Strategic Alignment:

A. Operational Execution

Policy & Process Documentation

- Update the policy and process notes, highlighting the proposed changes.

- Clear documentation on classification criteria for IMB-enabled customers and customer categories (Financial vs Non-Financial).

System-related changes

- Revise BRDs, functional specifications, and LCR calculation engines to incorporate revised runoff rates and haircuts for G-Sec’s.

- End-to-end lifecycle: BRD → Development → UAT → Production rollout.

- Update LCR reporting templates, dashboards, and internal MIS.

Integration with broader risk management framework

- Incorporate revised assumptions into:

- Liquidity Stress Testing Models;

- Pillar II ICAAP assessments;

- Contingency Funding Plans.

- Recalibrate survival horizons and buffer triggers.

B. Strategic Realignment

Funding Strategy Reassessment

- Review retail and SMEs’ deposit segmentation — balance IMB penetration with stable funding needs. Evaluate if changes are required in the way offerings are currently positioned.

- Considering the lower runoff factor for certain non-financial entities, now Bank’s can actively pursue deposit mobilization from these customers to diversify its funding profile.

HQLA Recalibration & Capital Deployment

- Assess surplus in HQLA buffers under the proposed changes.

- Evaluate the release of liquidity after considering the risk appetite and deployment strategies into high-yielding assets.

Treasury Portfolio Optimization

- Rebalance SLR portfolio to manage yield vs haircut trade-offs.

- Realign duration and issuer profile (Central Government vs State Government) of securities to optimize HQLA composition.

Strategic ALCO & FTP Realignment

- ALCO packs to be updated with revised numbers and the liquidity costs.

- FTP framework needs to be updated considering the liquidity cost and change in the funding strategy.

- Incentivize business units for sourcing “LCR-favorable” liabilities.

Final Thoughts

These changes are a big step toward making the LCR framework more practical and risk-sensitive. While Banks will need to do some significant groundwork over the next year, such as updating their systems, policies, and how they evaluate and assess customer behavior, there’s also a real opportunity to optimise HQLA and freeing up the liquidity to deploy funds where they can meaningfully impact the bottom line.